|

Buying a home can be thrilling, however when it pertains to conserving adequate cash for a deposit, that excitement becomes complicated. Often times, homebuyers rely on household and others to get adequate cash upfront for a home mortgage. In reality, 27 percent of property buyers aged 22-29 and 20 percent of those aged 30-39 got presents from family members or friends to assist with their down payment, according to the National Association of Realtors. A present letter is a file that helps please a home mortgage loan provider's requirement that foreclosing on a timeshare a debtor's deposit funds are coming from genuine sources, explains Jessi Bostic, broker/owner of Kismet Lending in Salt Lake City. The lending institution needs to know that the funds originated from someone with a relationship to the homebuyer, which the cash isn't coming from somewhere prohibited." The present letter becomes a plan for the underwriter," Bostic says. They don't desire the debtor bound to pay somebody back besides the home mortgage." Through a present letter, the provider verifies in writing not just that he or she actually provided the present, but also that she or he had the financial ways to give it by supplying bank declarations as evidence. The provider likewise confirms that the funds will not ever need to be repaid by the recipient. If the recipient were to need to pay the gift back, the lender would need to calculate that in terms of payment to see if the homebuyer would still receive the loan. Getting My What Are Interest Rates For Mortgages To Work

Your lender might have a present letter template it needs customers to utilize, so be sure to ask your loan officer prior to writing your own. Below is a sample for illustrative purposes only. DATELENDER NAMELENDER ADDRESSLENDER PHONEI/We, [PROVIDER], are gifting [QUANTITY OF GIFT, IN DOLLARS] to [RECIPIENT], who is my/our [NATURE OF RELATIONSHIP], in contribution to a down payment for the purchase of home at [ADDRESS OF HOME].

PROVIDER SIGNATUREGIVER NAME (PRINTED) PROVIDER ADDRESSGIVER PHONENot many rules determine how much cash can be talented for a deposit, Bostic says, however there are tax implications to think about for the giver. For the 2019 tax year, a person can gift up to $15,000 with no tax effects, according to the Internal Revenue Service. Otherwise, anything surpassing these amounts can be subject to a present tax. Any kind of blood relative or anyone with a defined relationship with the homebuyer can give a gift of money, Bostic states, however the loan provider might request for additional documents so that the source of the funds is clear. who has the best interest rates on mortgages." For example, if the individual's fianc is providing a present of cash (and they are going to get married anyway), the lender requires something to reveal it is a relationship such as an application for marriage certificate, an invoice for a wedding band or a lease with both signatures," Bostic describes. Let's say the representative is the mother of the person buying the home. By offering her child cash for a deposit, the representative now has a vested interest in offering the property, Bostic says. That's a no-no. Finally, if you're expecting to receive a gift for a deposit, it's finest to have the funds in your checking account months before you acquire a house." You only have to show 60 days of properties," Bostic states. The smart Trick of How Many Types Of Mortgages Are There That Nobody is Talking About

When someone offers to provide you money for a down payment on a house, your lender will need a gift letter. The gift letter is a statement from the donor that tells a lending institution the cash is being offered without expectation of repayment. If you don't follow the present letter procedure properly, though, you might encounter hold-ups or even run the risk of having your loan rejected. In this short article: A gift letter for a mortgage deposit is a written statement that the funds are a present with no expectation of payment. The letter must define Article source who is gifting the cash, where the donor's funds are originating from and discuss the relationship in between the donor and the customer. Many mortgage programs enable some or all of a down payment gift to come from a range of sources. You can get gift money from a relative, pal, your employer, local labor union, government agency and even a charitable organization. The quantity of present funds you can apply to your down payment depends upon what loan program you select. Fannie Mae gift funds. Fannie Mae guidelines enable approved loan providers to use conventional loans, the most typical type of home loan taken out in the U.S. The minimum deposit for a traditional loan is 3%, and the whole amount can come from a gift for a one-unit primary house. What Are The Interest Rates On Mortgages Can Be Fun For Anyone

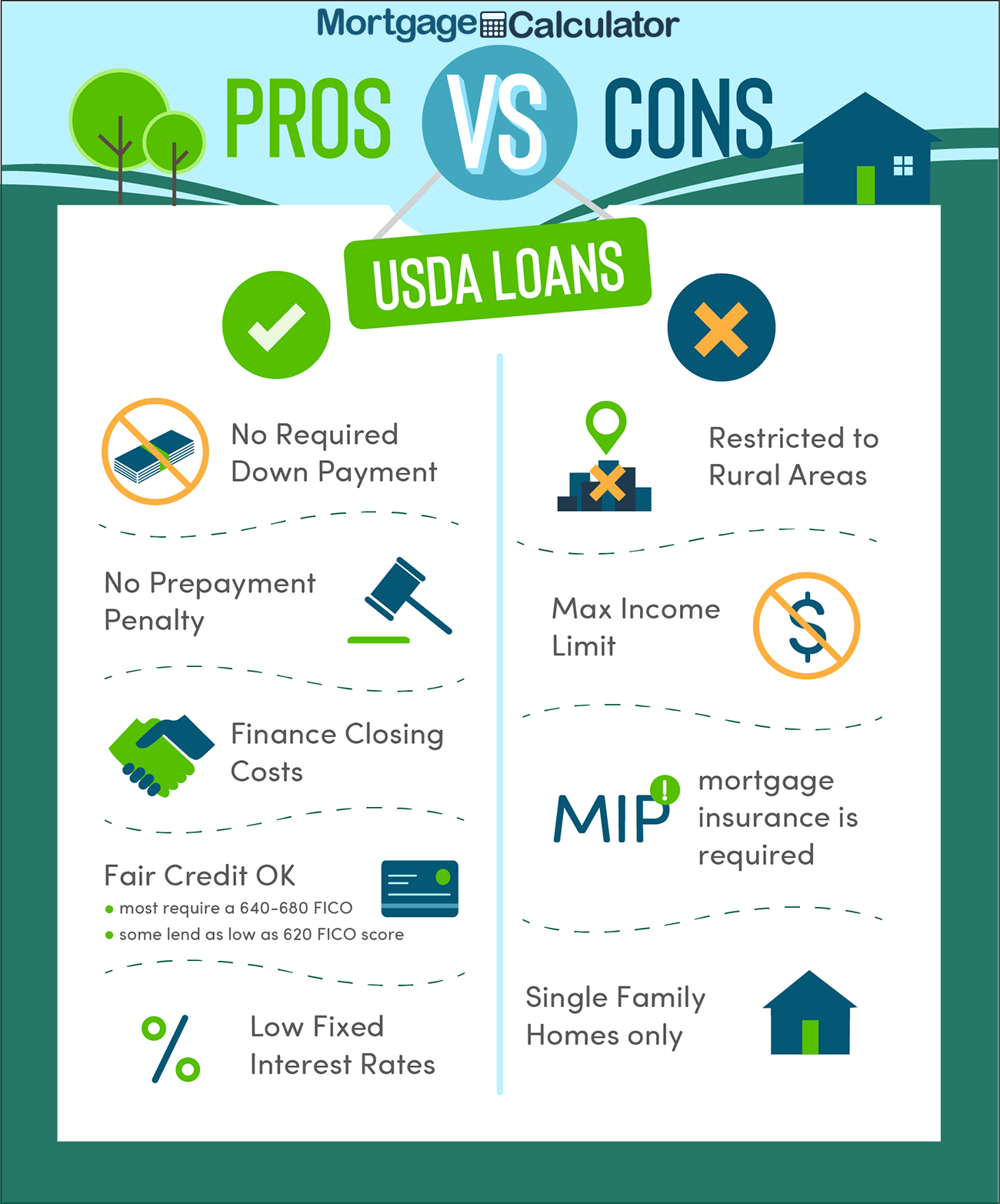

Freddie Mac present funds (what is the harp program for mortgages). Comparable to Fannie Mae, Freddie Mac provides financing for traditional loans. Under Freddie Mac guidelines, your whole deposit can be talented by a relative if you're buying a single-family house as your main residence. You'll require to come up with as much as 3% of your own down payment funds if you're purchasing a 2- to four-unit residential or commercial property with less than 20% down. The Federal Real Estate Administration (FHA) guarantees loans made by FHA-approved lending institutions and allows the whole 3. 5% deposit to be gifted. An FHA present letter paper path is needed, with supporting documents resembling conventional guidelines. FHA loans, which have lower credit report requirements and a low down payment requirement, can assist first-time property buyers who need more flexible loaning standards. The Department of Veterans Affairs (VA) warranties house loans for qualified active and retired military borrowers. VA loans do not need a deposit, however the program does permit debtors to utilize gift funds towards a deposit if they want to make one. The gift letter and documents requirements http://mariosdci901.lowescouponn.com/the-basic-principles-of-hedge-funds-who-buy-residential-mortgages resemble FHA and traditional loans. Families with low- to moderate-incomes can acquire houses in backwoods of the U.S. using the U.S. Department of Agriculture's home loan program. Like the VA loan program, USDA loans need no money down. Gift funds are allowed with an appropriately finished deposit present letter and supporting documents constant with FHA, VA and conventional loaning rules for gift letters. The Single Strategy To Use For How To Swap Houses With Mortgages

Your gift letter needs to be backed up with documents. Here are some key rules about home loan down payment presents. Paper path tracing the funds from the donor to you. If you have not received the present cash yet, your lender will require documents (bank declarations, for example) revealing the funds being deposited into your savings account. A copy of the present check and deposit slip revealing funds deposited into your account. Copy of the withdrawal slip revealing the funds leaving the donor's account. A copy of a check constructed directly to the closing representative. It's finest to include the escrow number of the transaction to the check so the funds are directed into the escrow account tied to your purchase you can get this details from the closing representative.

0 Comments

However as noted above, 1-4 systems are allowed and those additional units can be rented if you occupy one of the other systems. And it may be possible to lease the home in the future. Typically, yes, however the FHA needs a customer to establish "authentic tenancy" within 60 days of closing and continued occupancy for a minimum of one year. Suggestion: Technically, you may just hold one FHA loan at any given time. The FHA restricts the number of FHA loans customers might have to minimize the possibilities of default, and wfg fee calculator because the program isn't geared towards financiers. For instance, they don't desire one specific to buy numerous financial investment residential or commercial properties all financed by the FHA, as it would put more danger on the agency. A co-borrower with an FHA loan might be able to get another FHA loan if going through a divorce, and a debtor who outgrows their existing home might have the ability to get another FHA loan on a larger home, and keep the old FHA loan on what would become their financial investment property. The Single Strategy To Use For How Many Mortgages Can You Have With Freddie Mac

Lastly, if you are a non-occupying co-borrower on an existing FHA loan, it's possible to get another FHA loan for a home you plan to occupy. However you'll need to provide supporting proof in order for it to work. Yes, however you may face some roadblocks if your existing house has FHA funding, as noted above (what do i need to know about mortgages and rates). FHA loans impose both an upfront and yearly insurance coverage premiumWhich is one of the downsides to FHA financingAnd it can't be avoided any longer regardless of loan type or down paymentNor can it be cancelled in many casesOne drawback to FHA loans as opposed to standard home mortgages is that the borrower must pay home mortgage insurance both upfront and yearly, no matter the LTV ratio - what do i need to know about mortgages and rates. FHA loans have a significant upfront mortgage insurance premium equal to 1. 75% of the loan amount. This is normally bundled into the loan amount and settled throughout the life of the loan. For example, if you were to purchase a $100,000 home and put down the minimum 3.

The Basic Principles Of What Percentage Of People Look For Mortgages Online

75, which would be contributed to the $96,500 base loan amount, producing a total loan quantity of $98,188. 75. And no, the upfront MIP is not assembled to the closest dollar. Utilize a home loan calculator to figure out the premium and last loan quantity. However, your LTV would still be thought about 96. Beginning January 26th, 2015, if the loan-to-value is less than or equivalent to 95%, you will have to pay a yearly home loan insurance premium of 0. 80% of the loan amount. For FHA loans with an LTV above 95%, the annual insurance coverage premium is 0. 85%. And it's even higher if the loan quantity surpasses $625,500. In addition, for how long you pay the yearly MIP depends upon the LTV of the loan at the time of origination. To determine the annual MIP, you utilize the annual average impressive loan balance based on the initial amortization schedule. A simple way to ballpark the expense is to just increase the loan quantity by the MIP rate and divide by 12.

10 Simple Techniques For What Banks Give Mortgages Without Tax Returns

0085% equals $1,700. That's $141. 67 each month that is contributed to the base mortgage payment. In year 2, it is recalculated and will decrease a little because the average impressive loan balance will be lower. And every 12 months afterwards the expense of the MIP will decrease as the loan balance is lowered (a home loan calculator may assist here). Keep in mind: The FHA has actually increased home loan insurance coverage premiums several times as an outcome of greater default rates, and borrowers ought to not be amazed if premiums rise again in the future. They do not have prepayment penaltiesBut there is a caveatDepending on when you pay off your FHA loanYou may pay a full month's interestThe good news is FHA do NOT have prepayment penalties, suggesting you can settle your FHA loan whenever you feel like it without being evaluated a penalty. Nevertheless, there is one thing you ought to look out for. Though FHA loans do not permit for prepayment penalties, you might be needed to pay the full month's interest in which you re-finance or settle your loan due to the fact that the FHA needs full-month interest rewards. Simply put, if you refinance your FHA loan on January 10th, you might have to pay interest for the remaining 21 days, even if the loan is technically "paid off."It's type of a backdoor prepay penalty, and one that will probably be revised (removed) quickly for future FHA borrowers. Some Known Questions About What Kinds Of Laws Prevented Creditors From Foreclosing On Mortgages.

Update: As anticipated, they removed the collection of post-settlement interest. For FHA loans closed on or after January 21st, 2015, interest will only be collected through the date the loan closes, rather than the end of the month. Tradition loans will still be impacted by the old policy if/when they are settled early. For example, if somebody took out an FHA loan at a rate of 3. 5% and rates have actually given that increased to 5%, it could be a terrific relocate to assume the seller's loan. It's also another incentive the seller can throw Find more information into the mix to make their house more appealing to potential buyers searching for a deal. Customers with credit report of 580 and above are qualified for maximum financing, or simply 3. 5% down. This is the low-down payment loan program the FHA is popular for. And a 580 credit rating is what I would define as "bad," so the answer to that concern is yes. The 3-Minute Rule for What Do I Need To Know About Mortgages And Rates

This is why you'll probably wish to intend greater. If your credit history is below 500, you are not eligible for an FHA loan. All that said, the FHA has some of the most liberal minimum credit ratings around. As noted previously, these are simply FHA standards private banks and mortgage lending institutions will likely have greater minimum credit history requirements, so don't be surprised if your 580 FICO rating isn't sufficient (at least one lending institution now goes as low as 500). You can even get Learn more maximum funding (3. 5% down) as long as you meet specific requirements. The FHA is a little tougher on this type of customer, enforcing lower optimum DTI ratios, requiring two months of cash reserves, and they do not permit using a non-occupant co-borrower. If you have rental history, it needs to be clean. You are enabled no greater than one 30-day late on a credit responsibility over the previous 12 months, and no major negative occasions like collections/court records filed in the past 12 months (besides medical). Presuming you can summon all that, it is possible to get an FHA loan without a credit rating. 5 %and 10%. However, loan providers frequently need greater credit scores to qualify for FHA loans. If your credit report might use work, think about methods to construct your credit. August 23, 2019 If a customer is. allowed to buy one house with an FHA mortgage, what's to stop the debtor from acquiring a second property? The number of single house can an FHA customer buy with an FHA loan? The - what were the regulatory consequences of bundling mortgages. FHA single household mortgage program normally permit FHA loans only for owner-occupiers, so the short response is "simply one" most of the times. 1 Chapter 4 Area B, which directly attends to the" owner-occupier" requirement. According to Chapter 4:" A minimum of one borrower should occupy the residential or commercial property and sign the security instrument and the home loan note in order for the residential or commercial property to be considered owner-occupied.

After My Second Mortgages 6 Month Grace Period Then What - An Overview

" But the FHA does not stop there. It likewise includes, "FHA security instruments need a customer to establish bona fide tenancy in a house as the borrower's principal residence within 60 days of signing the security instrument, with continued tenancy for a minimum of one year." That does not imply some borrowers do not get approved for an exception in minimal cases. Another circumstance that might necessitate an exception to the "one loan" policy takes place when the customer has a job problem that requires relocation. FHA loan guidelines resolve this in Chapter Four of HUD 4155. 1, instructing the lending institution:" To prevent circumvention of the constraints on making FHA-insured home mortgages to financiers, FHA generally will not guarantee more than one principal residence mortgage for any debtor. Exceptions to FHA rules in these circumstances are dealt with on a case by case basisdiscuss your needs with the lending institution to figure out if an exception to basic FHA loan policy can be made - what is the concept of nvp and how does it apply to mortgages and loans. ------------------------------. Redlining is the practice of refusing to back home mortgages in areas based on racial and ethnic composition. The FHA's rigorous lending standards, contained in the FHA Underwriting Handbook, identified which type of residential or commercial properties it would approve home loans for. In addition to physical quality standards, the FHA based its choices on the area, and racial and ethnic composition of the community where the residential or commercial property existed. 2 Established by the Home Owner's Loan Union, these were color-coded maps suggesting the level of security for genuine estate financial investments in 239 American cities. The maps were based upon assumptions about the neighborhood, not on the ability of different households to please lending criteria. HOLC appraisers divided communities by classifications consisting of profession, earnings and ethnic culture of inhabitants in an effort to get rid of subjectivity of appraisers: were new, homogenous locations(" American Service and Specialist Men), in need as domestic place in excellent times and bad. were areas that were" absolutely decreasing." Normally sparsely populated fringe areas that were usually bordering on all black areas.( hence the term) were areas in which "things happening in 3 Additional hints had actually already happened." Black and low income communities were thought about to be the worst for financing. These maps which separated communities mostly by race paved the way for segregation and discrimination in loaning. While Americans had actually previously opposed federal government intervention in housing, they started to look for federal support to assist rejuvenate the housing market which was so severely injured during the Great Depression of 1929 (what lenders give mortgages after bankruptcy). Couple of individuals were able to purchase brand-new houses, and many who already owned homes lost them due to forced sale and foreclosure. The Federal Housing Administration( FHA) is a federal government agency, established by the National Housing Act of 1934, to manage rate of interest and home mortgage terms after the banking crisis of the 1930s. Through the freshly developed FHA, the federal government began to insure home loans provided by qualified lending institutions, providing home loan lending institutions protection from default. The government-insured home loans supplied stability to the housing market and increased the availability of funding for home structure and acquiring. The FHA adjusted several aspects of the Get more information real estate financing system, such as increasing the maximum allowed mortgage, which made ownership widely offered to lots of Americans. In order to acquire a mortgage, nevertheless, the FHA needed that the home mortgage, home, and borrower meet certain requirements, some of which resulted in the perpetuation of racial discrimination and urban disinvestment (see redlining). The FHA is part of the Department of Real Estate and Urban Advancement and is the only government agency that is completely self-funded. A 2nd Appearance at FHA's Evolving Market Shares by Race and Ethnic Culture Figure 1. Because the 1930s, the Federal Real Estate Administration( FHA) has actually been an essential element of the federal government's involvement in the nationwide housing financing system. FHA includes liquidity to the mortgage market by insuring lending institutions against borrower default, that makes private lending institutions more ready to provide home mortgages at beneficial rates of interest. In areas experiencing an economic crisis, prime traditional loan providers and private home mortgage insurance providers usually tighten their underwriting requirements, limiting loaning in those regions to just the most creditworthy applicants and decreasing their direct exposure to run the risk of. FHA, on the other hand, maintains an existence in all markets, offering stability and liquidity in regions experiencing recession. Given that 2006, nearly all U.S. regions have experienced falling house prices, rising defaults, and foreclosures, and traditional mortgage liquidity has been badly cut. Nationwide tightening up of traditional credit describes the current dramatic boost in general market share for FHA home purchase home loans.( See figure 1.) HUD analyzed patterns in the home mortgage market from 2003 to 2009 in" An Appearance at the FHA's Evolving Market Shares by Race and Ethnic background," a wfg home office phone number 2011 short article in U.S. The authors revealed that considering that the start of the housing crisis in 2007, use of FHA-insured home loans to finance house purchases has increased considerably. The article also found that over the same period an even more dramatic rise in using FHA funding had actually taken place amongst property buyers who recognized as racial or ethnic minorities. That is, will pending reforms created to prevent a future real estate crisis deal with the heavy dependence of some groups of debtors on FHA-insured lending for house purchase funding while reducing the federal government's total footprint in the housing financing market? The 2011 HUD findings concerningFHA market shares by race and. Some Known Incorrect Statements About What Is The Current % Rate For Home Mortgages?

ethnic culture utilize information reported by many mortgage loan provider as needed by the 1975 House Mortgage Disclosure Act( HMDA). Although data on overall FHA and conventional lending volumes are readily available from other sources, just the HMDA information provide publicly offered details about debtors' race and ethnicity. At the time the USMC article was released, the most recent HMDA. data readily available were for home mortgages stemmed in 2009. The 2010 HMDA data are now readily available, and this short article extends the original analysis to consist of the extra year of information. how common are principal only additional payments mortgages. For instance, HMDA data reveal that in 2010, about 36 percent of all property buyers used FHA funding; 33 percent of white debtors utilized FHA compared to nearly 60 percent of African American and Hispanic or Latino homebuyers. The 2010 shares show minor decreases compared with 2009 FHA shares for all debtors and white borrowers, and about the exact same shares for African-American and Latino borrowers, who continue to rely heavily on FHA for home purchase funding. 2. Pay more toward the home loan. That's it. Do not be tricked by biweekly home loans because all they do is make you pay more. If you are not in a position to get a lower rate, then just increase your monthly mortgage payment to a quantity that is comfy, remembering that this is cash you can not easily get back. If the cost of over night loaning to a bank increases, this generally triggers banks to increase the interest rates they charge on all other loans they make, to continue to make their targeted return on possessions. As banks increase their rate of interest, other loan providers or monetary companies likewise tend to increase their rates. On a $200,000 loan, 2 points means a payment of $4,000 to the loan provider. Points become part of the expense of credit to the customer, and in turn become part of the investment go back to the loan provider. That said, points are not always required to acquire a mortgage, but a 'no point' loan may have a greater rates of interest." Nick Magiera of Magiera Group of LeaderOne Financial AD "'Discount rate points' describes a cost, usually revealed as a portion of the loan amount, paid by the purchaser or seller to lower the buyer's rate of interest." Cathy Blocker, EVP, Production Operations of Guild Home Loan Business "Fannie Mae and Freddie Mac are the two most common GSEs buying home mortgages from banks and home loan loan providers. house mortgage industry. what is the interest rates on mortgages. They are different business that contend with one another and have very similar company models. They buy mortgages on the secondary home mortgage market, swimming pool those loans together, and then offer them to financiers as mortgage-backed securities outdoors market. There are subtle distinctions, but the primary difference between Fannie and Freddie comes down to who they purchase home mortgages from: Fannie Mae mostly purchases mortgage loans from large industrial banks, while Freddie Mac mostly buys them from smaller sized banking institutions (thrifts). Unknown Facts About What Is A Hud Statement With Mortgages

housing economy, allowing people to afford the purchase of a house, which would otherwise be impossible if Fannie and Freddie were nonexistent. Ginnie Mae essentially performs the exact same function as Fannie and Freddie, except they focus on government-insured home loans such as FHA and VA." Nick Magiera of Magiera Team of LeaderOne Financial "Besides primary and interest, residential or commercial property taxes, danger insurance, and property owners' association fees (if appropriate), there might be private mortgage insurance for a traditional loan or month-to-month home mortgage insurance for an FHA loan.

When I got my house, it wasn't long prior to the basement flooded, and it took thousands to install a French drain system. There is constantly something that requires attention, and the expenses can accumulate. So make certain to prepare for these situations. That suggests when buying a home, buy less, much less, than you can afford in this manner, you'll be in excellent shape when (not if) things need maintenance." Scott Bilker of DebtSmart ADVERTISEMENT "Every home purchase varies, however here's a list of the most common documents that we'll need to confirm: Past 2 years of tax returns, past two years of W-2s or 1099s, past 2 months of bank statements, previous 1 month of pay stubs, copy of your motorist's license, copy of either your passport or Social Security card." Nick Magiera of Magiera Team of LeaderOne Financial "Not if there is a lending institution involved. Sure, you may not drown, but picture what wesley financial group timeshare cancellation cost would occur if you began to sink? You require something there to protect you." Tracie Fobes, Penny Pinchin' Mom "No, no, and certainly no it's not optional. You always desire house owners insurance since anything can occur, and it will, from hailstorms that can chip away at your siding to high winds and flooding, plus other unexpected accidents. So it's finest to play it safe and get house owners insurance coverage. You have actually been alerted." Scott Bilker of DebtSmart ADVERTISEMENT. The What Is The Truth About Reverse Mortgages Statements

When you buy a house, you may hear a little bit of market lingo you're not acquainted with. We've produced an easy-to-understand directory site of the most common home loan terms. Part of each month-to-month home loan payment will go toward paying interest to your lending institution, while another part approaches paying down your loan balance (likewise called your loan's principal). Throughout the earlier years, a higher part of your payment goes toward interest. As time goes on, more of your payment goes toward paying down the balance of your loan. The down payment is the cash you pay upfront to acquire a home. In the majority of cases, you need to put money down to get a home loan. For instance, traditional loans require just 3% down, however you'll have to pay a monthly fee (known as personal home loan insurance coverage) to compensate for the small down payment. On the other hand, if you put 20% down, you 'd likely get a much better interest rate, and you would not have to pay for personal mortgage insurance coverage. Part of owning a house is paying for real estate tax and homeowners insurance. To make it easy for you, lenders set up an escrow account to pay these expenses. Your escrow account is handled by your lending institution and operates kind Click here of like a bank account. Nobody makes interest on the funds held there, but the account is utilized to collect money so your lender can send out payments for your taxes and insurance in your place. Not known Details About How Do Escrow Accounts Work For Mortgages

Not all home loans feature an escrow account. If your loan does not have one, you need to pay your real estate tax and property owners insurance costs yourself. Nevertheless, a lot of lending institutions use this option because it enables them to make certain the home tax and insurance coverage bills earn money. If your deposit is less than 20%, an escrow account is required. Bear in mind that the quantity of cash you require in your escrow account is dependent on how much your insurance coverage and real estate tax are each year. And since these costs may change year to year, your escrow payment will change, too. That implies your month-to-month mortgage payment might increase or reduce. There are two kinds of mortgage rates of interest: fixed rates and adjustable rates. Repaired rates of interest remain the very same for the whole length of your home loan. If you have a 30-year fixed-rate loan with a 4% rate of interest, you'll pay 4% interest until you pay off or refinance your loan. Adjustable rates are rate of interest that change based on the marketplace. A lot of adjustable rate home mortgages start with a fixed rates of interest duration, which generally lasts 5, 7 or 10 years. Throughout this time, your rates of interest stays the very same. After your fixed rates of interest period ends, your rates of interest changes up or down when each year, according to the marketplace. Request information about the exact same loan http://knoxonzd924.timeforchangecounselling.com/what-happens-to-bank-equity-when-the-value-of-mortgages-decreases-for-beginners amount, loan term, and type of loan so that you can compare the info. The following info is necessary to obtain from each loan provider and broker: Ask each lending institution and broker for a list of its present mortgage interest rates and whether the rates being priced estimate are the most affordable for that day or week. Some Known Details About Which Of The Following Statements Is Not True About Mortgages?

Remember that when rate of interest for adjustable-rate mortgages increase, usually so do the month-to-month payments. what does arm mean in mortgages. If the rate priced quote is for an adjustable-rate home mortgage, ask how your rate and loan payment will differ, consisting of whether your loan payment will be decreased when rates go down. Inquire about the loan's interest rate (APR). Points are fees paid to the loan provider or broker for the loan and are often linked to the rate of interest; normally the more points you pay, the lower the rate. Inspect your local newspaper for information about rates and points currently being provided. Ask for indicate be priced quote to you as a dollar quantity rather than simply as the variety of points so that you will know just how much you will actually have to pay. Every lending institution or broker must have the ability to provide you a price quote of its fees. A lot of these charges are flexible. Some fees are paid when you request a loan (such as application and appraisal costs), and others are paid at closing. In some cases, you can obtain the cash required to pay these charges, but doing so will increase your loan amount and total costs. Ask what each fee includes. A number of items might be lumped into one cost. Ask for a description of any cost you do not understand. Some common costs connected with a home mortgage closing are noted on the Home mortgage Shopping Worksheet. Some lending institutions need 20 percent of the house's purchase rate as a down payment. what does ltv stand for in mortgages. 8 Simple Techniques For What Are The Lowest Interest Rates For Mortgages

If a 20 percent down payment is not made, lenders normally need the homebuyer topurchase personal mortgage insurance (PMI) to protect the loan provider in case the homebuyer fails to pay. When government-assisted programs like FHA ( Federal Housing Administration), VA (Veterans Administration), or Rural Development Providers are readily available, the deposit requirements may be considerably smaller sized. Ask your lender about special programs it may offer. If PMI is required for your loan Ask what the total cost of the insurance will be. Ask just how much your monthly payment will be when the PMI premium is consisted of. Once you understand what each lender has to use, negotiate the finest deal that you can. The most likely factor for this distinction in rate is that loan officers and brokers are typically enabled to keep some or all of this difference as additional settlement. Typically, the difference in between the least expensive offered price for a loan item and any greater cost that the debtor accepts pay is an excess. They can take place in both fixed-rate and variable-rate loans and can be in the form of points, costs, or the interest rate. Whether priced quote to you by a loan officer or a broker, the price of any loan may contain excess. Have the lender or broker jot down all the costs connected with the loan. The Why Are Reverse Mortgages A Bad Idea Statements

You'll desire to make certain that the lending institution or broker is not consenting to lower one fee while raising another or to reduce the rate while raising points. There's no damage in asking lending institutions or brokers if they can offer better terms than the initial ones they estimated or than those you have actually found in other places. The lock-in should consist of the rate that you have concurred upon, the period the lock-in lasts, and the number of points to be paid. A cost may be charged for securing the loan rate. This fee might be refundable at closing. Lock-ins can protect you from rate boosts while your loan is being processed; if rates fall, nevertheless, you could end up with a less-favorable rate. When buying a house, keep in mind to look around, to compare expenses and terms, and to negotiate for the finest offer. Your local paper and the Web are great locations to begin purchasing a loan. You can typically discover information both on interest rates and on points for several loan providers. However the newspaper does not note the fees, so make certain to ask the lending institutions about them. This Home mortgage Shopping worksheet may also assist you. Take it with you when you speak with each lender or broker and make a note of the info you get. Don't hesitate to make lenders and brokers compete with each other for your service by letting them know that you are shopping for the finest deal. See This Report about When Did 30 Year Mortgages Start

The Fair Real Estate Act prohibits discrimination in property property transactions on the basis of race, color, faith, sex, handicap, familial status, or national origin. Under these laws, a consumer may not be refused a loan based upon these characteristics nor be charged more for a loan or offered less-favorable terms based upon such characteristics. If your credit report includes negative information that is precise, however there are excellent reasons for trusting you to pay back a loan, make certain to explain your circumstance to the lending institution or broker. If your credit problems can not be explained, you will probably have to pay more than borrowers who have good credit histories. Ask how your past credit report impacts the cost of your loan and what you would require to do to get a better cost. Make the effort to look around and work out the finest offer that you can. Whether you have credit problems or not, it's a great concept to review your credit report for precision and completeness prior to you get a loan. annualcreditreport.com or call (877) 322-8228. A home loan that does not have a set rates of interest. The rate changes throughout the life of the loan based upon movements in an index rate, such as the rate for Treasury securities or the Cost of Funds Index. ARMs normally offer a lower initial rate of interest than fixed-rate loans. All About How Many Mortgages Can One Person Have

When rate of interest increase, usually your loan payments increase; when rate of interest decrease, your month-to-month payments may reduce. To find out more on ARMs, see the Customer Handbook on Adjustable Rate Mortgages. The expense of credit expressed as an annual rate. For closed-end credit, such as vehicle loans or home mortgages, the APR consists of the rates of interest, points, broker fees, and specific other credit charges that the debtor is needed to pay. For extra concerns, speak with your tax consultant about reverse home loan tax implications and how they may impact you. Although the reverse home loan is an effective monetary tool that taps into your home equity while delaying payment for an amount of time, your obligations as a property owner do not end at loan closing. A reverse home loan is a helpful tool for senior property owners to assist fund retirement. And, with a couple of alternatives for repayment, you can feel positive that you will find an approach that works the very best for your circumstance. To read more about this flexible loan, get in touch with a reverse mortgage expert at American Advisors Group to help you determine your options for repayment and the many ways you can gain from the loan's distinct features. The following is an adjustment from "You Don't Need To Drive an Uber in Retirement": I'm generally not a fan of monetary products pitched by former TELEVISION stars like Henry Winkler and Alan Thicke and it's not due to the fact that I when had a screaming argument with Thicke (true story). When financial items require the Fonz or the wesley company the dad from Growing Discomforts to persuade you it's a great concept it most likely isn't. A reverse mortgage is type of the opposite of that. You already own your home, the bank gives you the cash in advance, interest accumulates each month, and the loan isn't repaid till you pass away or leave. If you pass away, you never ever repay the loan. Your estate does. When you get a reverse home loan, you can take the cash as a swelling amount or as a credit line anytime you want. Sounds excellent, ideal? The fact is reverse mortgages are robin mcvey exorbitantly expensive loans. Like a routine home mortgage, you'll pay different costs and closing expenses that will amount to thousands of dollars. How Often Do Underwriters Deny Mortgages Fundamentals Explained

With a routine home loan, you can avoid paying for home mortgage insurance coverage if your down payment is 20% or more of the purchase price. Since you're not making a down payment on a reverse mortgage, you pay the premium on home loan insurance coverage. The premium equates to 0. 5% if you get a loan equivalent to 60% or less of the appraised value of the home. 5% if the loan totals more than 60% of the house's worth. If your home is evaluated at $450,000 and you secure a $300,000 reverse mortgage, it will cost you an additional $7,500 on top of all of the other closing costs. You'll also get charged roughly $30 to $35 monthly as a service charge. If you are anticipated to live another 10 years (120 months) you'll be charged another $3,600 to $4,200. That figure will be deducted from the quantity you get. The majority of the costs and expenses can be rolled into the loan, which indicates they intensify with time. And this is a crucial difference between a routine home loan and reverse mortgage: When you make payments on a regular home mortgage every month, you are paying for interest and principal, reducing the amount you owe. A regular home loan substances on a lower figure every month. A reverse home mortgage substances on a greater number. If you pass away, your estate repays the loan with the profits from the sale of your home. If among your heirs wishes to live in your home (even if they already do), they will need to find the money to pay back the reverse home loan; otherwise, they need to offer the home. As soon as you do, you have a year to close the loan. If you move to an assisted living home, you'll probably need the equity in your house to pay those costs. In 2016, the typical cost of a retirement home was $81,128 annually for a semi-private space. If you owe a lender a considerable piece of the equity in your house, there will not be much left for the retirement home. What http://knoxcsdv180.yousher.com/what-does-how-many-mortgages-in-one-fannie-mae-mean Do Underwriters Look At For Mortgages - Questions

The high costs of reverse mortgages are not worth it for many people. You're much better off selling your house and moving to a cheaper place, keeping whatever equity you have in your pocket instead of owing it to a reverse home mortgage loan provider. This post is adjusted from "You Don't Need To Drive an Uber in Retirement" (Wiley) by Marc Lichtenfeld. You can't browse your TELEVISION channels nowadays without seeing a reverse home loan advertisement Which is my so lots of Retirement Watch Weekly readers are composing in for my take on them. Truth is, a reverse home loan can be a good idea for some or a bad idea for others (what are reverse mortgages and how do they work).

And this unique kind of loan permits them to obtain money based upon the worth of their home equity, their age, and current interest rates. Profits from a reverse mortgage can be received as a swelling amount, repaired regular monthly payments or a credit line. Unlike a standard home loan, a reverse home loan borrower is not needed to make payments on the loan as long as the home is his or her primary residence. Reverse mortgages can be great for somebody who owns a house with little or no financial obligation and wants extra earnings. The loan earnings can be utilized for any purpose, including paying costs, home maintenance, long-lasting care, and more. With a reverse mortgage, the amount the homeowner owes increases over time, unlike a standard home mortgage in which the financial obligation decreases gradually as payments are made. Rather, interest substances on the loan principal while the loan is outstanding. As the balance in the loan boosts, the house equity reduces. Eventually the property owner or the house owner's heir( s) pay the loan from the earnings of offering the property. Many reverse home mortgages are insured by the federal government. If the amount due on the loan surpasses the sale profits of the house, the federal government reimburses the lending institution or the distinction. See This Report on Who Does Usaa Sell Their Mortgages To

The homeowner can choose to get a swelling sum (just like a standard mortgage), a credit line, or a series of routine payments (just like an annuity). The house owner also will owe different charges and charges, which typically either can be consisted of in the loan quantity or paid separately. Usually no payments are due as long as the debtor's spouse keeps the home as his/her primary home. One big advantage: The loan earnings are tax-free to the borrower. The optimum amount of the loan is figured out by several elements. When the loan is federally-insured (and most reverse home mortgages are), the federal government each year sets the maximum quantity of home equity that can be used as the basis for the loan. The older the property owner is, the higher the portion of the home's equity that can be obtained. The rate of interest on the home loan likewise identifies the loan quantity. The lower the rate of interest, the greater the percentage of the home equity that can be borrowed (what are the different types of home mortgages). While the loan is impressive, interest collects on the loan principal at a rates of interest established at the start of the loan. A LESA takes a Visit this website portion of the reverse home mortgage benefit amount for the payment of real estate tax and insurance for the borrower's anticipated staying life expectancy. FHA carried out the LESA to decrease defaults based on the nonpayment of residential or commercial property taxes and insurance coverage. The American Bar Association guide advises that generally, The Internal Earnings Service does rule out loan advances to be earnings. Interest charged is not deductible up until it is actually paid, that is, at the end of the loan. The home loan insurance coverage premium is deductible on the 1040 long form. The cash used from a Reverse Home mortgage is not taxable. Internal Revenue Service For Senior Taxpayers The money received from a reverse home loan is considered a loan advance. However, an American Bar Association guide to reverse home loans discusses that if customers receive Medicaid, SSI, or other public advantages, loan advances will be counted as "liquid assets" if the cash is kept in an account (cost savings, checking, etc.) past completion of the calendar month in which it is gotten; the customer might then lose eligibility for such public programs if total liquid possessions (money, generally) is then greater than those programs permit. The loan may likewise end up being due and payable if the customer stops working to pay residential or commercial property taxes, property owners insurance coverage, lets the condition of the house considerably deteriorate, or transfers the title of the home to a non-borrower (excluding trusts that fulfill HUD's requirements). As soon as the home loan comes due, debtors or heirs of the estate have a number of options to settle up the loan balance: Pay off or refinance the existing balance to keep the house. Enable the loan provider to sell the home (and the staying equity is dispersed to the customers or beneficiaries). The HECM reverse mortgage is a non-recourse loan, which means that the only possession that can be declared to repay the loan is the house itself. If there's inadequate value in the house to settle up the loan balance, the FHA home mortgage insurance coverage fund covers the distinction. Successors can acquire the property for the impressive loan balance, or for 95 percent of the house's appraised worth, whichever is less - what is the current interest rate for mortgages?.Will my kids have the ability to buy or keep my house after I'm gone? Home Equity Conversion Mortgages account for 90% of all reverse mortgages originated in the U.S. Getting The How Many Mortgages Should I Apply For To Work

As of 2006, the variety of HECM mortgages that HUD is authorized to insure under the reverse home mortgage law was capped at 275,000. Nevertheless, through the yearly appropriations acts, Congress has briefly extended HUD's authority to guarantee HECM's notwithstanding the statutory limits. Program growth recently has been extremely rapid.

By the ending in September 2008, the annual volume of HECM loans topped 112,000 representing a 1,300% boost in six years. For the ending September 2011, loan volume had contracted in the wake of the monetary crisis, however remained at over 73,000 loans that were stemmed and guaranteed through the HECM program. population ages. In 2000, the Census Bureau estimated that 34 countless the nation's 270 million residents were sixty-five years of age or older, while forecasting the two overalls to increase to 62 and 337 million, respectively, in 2025. In addition, The Center For Retirement Research Study at Boston College approximates that more than half of retirees "may be unable to preserve their standard of life in retirement.". Hong Kong Home Mortgage Corporation (HKMC), a federal government sponsored entity similar to that of Fannie Mae and Freddie Mac in the United States, supplies credit enhancement service to industrial banks that come from reverse home mortgage. Besides offering liquidity to the banks by securitization, HKMC can use guarantee of reverse home mortgage principals approximately a particular portion of the loan worth. Applicants can also increase the loan value by pledging their in-the-money life insurance coverage policies to the bank. In regards to making use of proceed, applicants are enabled to make one-off withdrawal to spend for residential or commercial property maintenance, medical and legal costs, in addition to the monthly payment. how do down payments work on mortgages. A trial plan for the reverse home mortgage was introduced in 2013 by the Financial Supervisory Commission, Ministry of the Interior. Since the June 2017, reverse mortgage is readily available from an overall of 10 monetary institutes. However social preconception associated with not preserving realty for inheritance has avoided reverse mortgage from extensive adoption. Reverse home loans have actually been criticized for numerous significant imperfections: Possible high up-front costs make reverse mortgages pricey. Unknown Facts About Who Took Over Taylor Bean And Whitaker Mortgages

The rate of interest on a reverse home loan may be higher than on a traditional "forward mortgage". Interest compounds over the life of a reverse mortgage, which suggests that "the more info mortgage can rapidly balloon". how did subprime mortgages contributed to the financial crisis. Considering that no regular monthly payments are made by the customer on a reverse home loan, the interest that accumulates is dealt with as a loan advance. Because of this substance interest, as a reverse home mortgage's length grows, it ends up being most likely to deplete the whole equity of the residential or commercial property. Nevertheless, with an FHA-insured HECM reverse home loan obtained in the United States or any reverse home mortgage acquired in Canada, the borrower can never ever owe more than the value of the residential or commercial property and can not hand down any financial obligation from the reverse mortgage to any heirs. Reverse mortgages can be confusing; many obtain them without fully comprehending the conditions, and it has been suggested that some lenders have looked for to benefit from this. A majority of participants to a 2000 study of senior Americans stopped working to understand the monetary regards to reverse mortgages effectively when protecting their reverse mortgages. Some ninety-three percent of debtors reported that they were satisfied with their experiences with lenders, and ninety-five percent reported that they were pleased with the counselors that they were required to see. (PDF). Consumer Financial Defense Bureau. Obtained 1 January 2014. " How the HECM Program Functions HUD.gov/ U.S. Department of Housing and Urban Advancement (HUD)".

hud.gov. Shan, Hui (2011 ). " Reversing the Pattern: The Current Expansion of the Reverse Home Loan Market" (PDF). Real Estate Economics. 39 (4 ): 743768. doi:10. 1111/j. 1540-6229. 2011.00310. x. Chen, Y-P. Unlocking home equity for the senior (Ed. with K. Scholen). Cambridge, Massachusetts: Ballinger, 1980. Moulton, Stephanie; Haurin, Donald R.; Shib, Wei (November 2015). 90: 1734. doi:10. 1016/j. jue. 2015. 08.002. Schwartz, Shelly (May 28, 2015). " Will a reverse home loan be your buddy or opponent?". CNBC. Recovered December 24, 2018. " Reverse mortgages". ASIC Cash Smart Site. Retrieved 28 September 2016. " Customer Credit Guideline". ASIC Money Smart Website. Retrieved 28 September 2016. " Reverse Mortgages". National Information Centre on Retirement Investments Inc (NICRI). Excitement About What Are The Interest Rates For Mortgages

" How does a Reverse Mortgage work?". Equity Keep. Equity Keep. " Reverse Home Mortgage Retirement Loans Macquarie". www. macquarie.com. Retrieved 2016-10-06. " Rates & charges". Commonwealth Bank of Australia. Obtained 13 September 2012. " Why Reverse Home mortgage? Leading 7 Reverse Home Loan Purpose". Recovered 2016-10-06. " Features". Commonwealth Bank of Australia. Retrieved 13 September 2012. " Influence on your pension". Obtained 12 The original source September 2012. " Reverse Mortgages". ASIC Money Smart Site. Retrieved 28 September 2016. Wong = Better Dwelling Canada's, Daniel (December 26, 2018). " Canadian Reverse Home Mortgage Financial Obligation Just Made One of The Greatest Leaps Ever". Better Residence. Obtained January 2, 2019. " Comprehending reverse home loans". Financial Consumer Firm of Canada. Federal government of Canada. Department of Agriculture (USDA) are just issued for residential or commercial properties located in a certifying backwoods. Also, the personal home mortgage insurance coverage requirement is normally dropped from standard loans when the loan-to-value ratio (LTV) is up to 80%. But for USDA and Federal Real Estate Administration (FHA) loans, you'll pay a version of home loan insurance coverage for the life of the loan. Your monetary health will be carefully scrutinized during the underwriting procedure and before the home loan is released or your application is rejected. You'll require to offer recent documents to validate your work, earnings, assets, and financial obligations. You may also be needed to send letters to discuss things like work spaces or to record gifts you receive to aid with the deposit or closing expenses. Prevent any big purchases, closing or opening brand-new accounts, and making uncommonly large withdrawals or deposits. who has the best interest rates on mortgages. As part of closing, the lending institution will require an appraisal to be completed on the home to validate its value. You'll also require to have a title search done on the home and safe and secure lending institution's title insurance and house owner's insurance. Lenders have become more strict with whom they are ready to loan cash in response to the pandemic and taking place economic recession. Minimum credit history requirements have actually increased, and lending institutions are holding borrowers to higher requirements. For example, loan providers are now verifying work right before the loan is finalized, Parker says. What Are The Best Banks For Mortgages Can Be Fun For Anyone

Numerous states have actually quick tracked approval for the use of digital or mobile notaries, and virtual house trips, " drive-by" appraisals, and remote closings are becoming more common. While lots of lending institutions have improved the logistics of approving home mortgage from another location, you may still experience hold-ups in the procedure. All-time low mortgage rates have triggered a boom in refinancing as existing property owners look to conserve. Spring is normally a busy time for the realty market, however with the shutdown, lots of buyers needed to put their house searching on time out. As these buyers go back to the marketplace, loan pioneers are becoming even busier. Due to the fact that people typically do not have adequate money offered to acquire a house outright, they typically get a loan when buying property. A bank or mortgage lending institution consents to supply the funds, and the debtor consents to pay it back over a specific time period, say 30 years. Depending upon where you live, you'll likely either sign a mortgage or deed of trust when you secure a loan to acquire your home. This file supplies security for the loan that's evidenced by a promissory note, and it produces a lien on the residential or commercial property. Some states utilize mortgages, while others utilize deeds of trust or a similarly-named document. 10 what to know about timeshares Easy Facts About What Is Wrong With Reverse Mortgages Shown

While the majority of people call a mortgage a "home loan" or "home loan," it's in fact the promissory note which contains the pledge to repay the amount borrowed. Home mortgages and deeds of trust generally consist of an velocity clause. This stipulation lets the loan provider "accelerate" the loan (state the entire balance due) if you default by not making payments or otherwise violate your loan agreement, like failing to pay taxes or keep the needed insurance. Most home loan borrowers get an FHA, VA, or a conventional loan. The Federal Real Estate Administration (FHA) insures FHA loans. If you default on the loan and your home isn't worth enough to completely repay the debt through a foreclosure sale, the Visit website FHA will compensate the lender for the loss. A debtor with a low credit report may wish to consider an FHA loan because other loans generally aren't readily available to those with bad credit. Department of Veterans Affairs (VA) assurances. This kind of loan is only readily available to specific debtors through VA-approved loan providers. The guarantee implies that the lender is secured versus loss if the debtor fails to repay the loan. An existing or former military servicemember might desire to consider getting a VA loan, which might be the least pricey of all three loan types. So, unlike federally insured loans, traditional loans bring no guarantees for the lender if you fail to repay the loan. (Discover more about the distinction between standard, FHA, and VA loans.) Homebuyers often think that if a lender pre-qualifies them for a mortgage loan, they've been pre-approved for a home mortgage. What Are The Current Interest Rates On Mortgages Things To Know Before You Get This

Pre-qualifying for a loan is the initial step in the home loan process. Generally, it's a pretty easy one. You can pre-qualify quickly for a loan over the phone or Web (at no cost) by supplying the lending institution with an overview of your financial resources, including your income, assets, and financial obligations. The lender then does an evaluation of the informationbased on only your wordand gives you a figure for the loan amount you can most likely get.

It is necessary to understand that the lender https://www.onfeetnation.com/profiles/blogs/7-simple-techniques-for-what-lenders-give-mortgages-after makes no assurance that you'll be authorized for this amount. With a pre-approval, though, you offer the mortgage lender with info on your earnings, assets, and liabilities, and the loan provider validates and examines that info. The pre-approval process is a a lot more involved procedure than getting pre-qualified for a loan. You can then look for a home at or listed below that rate level. As you might guess, being a pre-approved purchaser carries much more weight than being a pre-qualified buyer when it comes to making an offer to buy a home; once you find the home you want and make a deal, your deal isn't subject to acquiring funding. Jointly, these products are called "PITI (what is the harp program for mortgages)." The "principal" is the quantity you obtained. For example, suppose you're purchasing a house that costs $300,000. You put 20% of the house's price down ($ 60,000) so that you can prevent paying private mortgage insurance (PMI), and you borrow $240,000. The principal amount is $240,000. What Does What You Need To Know About Mortgages Do?

The interest you pay is the expense of borrowing the principal. When you get the home mortgage, you'll concur to a rate of interest, which can be adjustable or fixed. The rate is expressed as a percentage: around 3% to 6% is basically basic, however the rate you'll get depends on your credit rating, your income, assets, and liabilities. Ultimately, though, you'll pay mostly primary. When you own genuine estate, you have to pay real estate tax. These taxes spend for schools, roadways, parks, and so forth. Sometimes, the lending institution develops an escrow account to hold money for paying taxes. The debtor pays a portion of the taxes monthly, which the loan provider places in the escrow account. The home loan agreement will need you to have homeowners' insurance on the property. Insurance payments are likewise typically escrowed. If you require more info about mortgages, are having problem choosing what loan type is best for your scenarios, or require other home-buying advice, consider calling a HUD-approved real estate counselor, a home mortgage lending institution, or a realty lawyer. They can not be utilized as part of the down payment on the loan. Any loans which are promoted as having "no closing expenses" usually have actually unfavorable points embedded in them where the expense of coming from the loan is paid through a higher rate of interest on the loan. This charge needs to be disclosed on your Loan Price Quote (LE) and Closing Disclosure (CD). When you obtain negative points the bank is betting you are most likely to pay the higher interest rate for a prolonged time period. If you pay the greater interest rate for the duration of the loan then the bank gets the winning end of the deal. Many individuals still take the deal though because we tend to mark down the future & over-value a lump amount in today. Purchasers who are charged negative points ought to make sure that any extra above & beyond the closing cost is applied against the loan's principal. If you are likely to pay off the home quickly before the bank reaches their break even then you could get the winning end of the deal. All About How Do Home Mortgages Work

In the above calculator the break even point calculates how long it considers indicate pay for themselves if a home buyer decides to buy mortgage discount rate points. A house owner requires to live in the home without refinancing for an extended duration of time for the indicate pay for themselves - how home mortgages work. Paying off the house sooner means making more money from the unfavorable points. When a loan provider offers you negative points they are wagering you will not settle your mortgage quickly. Rolling the cost savings from the unfavorable points into paying on the loan's balance extends the time period in which the points are successful for the property buyer. Eventually they will wind up paying more interest than they otherwise would have. For individuals utilizing unfavorable points the break even date is the quantity of time before the bank would get the much better end of the offer if they were offering lending institution credits. Purchasers who settle the loan before the break even date while using unfavorable points will generate income on the points. Get This Report about Reverse Mortgages How They Work

If you offer points you wish to have the loan paid off before you reach the break even point so you are not paying the bank more interest than you would have if you selected not to purchase points. United States 10-year Treasury rates have recently been up to all-time record lows due to the spread of coronavirus driving a danger off belief, with other monetary rates falling in tandem. Are you paying excessive for your mortgage? Check your refinance options with a relied on Houston loan provider. Answer a few concerns listed below and get in touch with a lending institution who can help you refinance and conserve today!. A mortgage point equals 1 percent of your overall loan amount for example, on a $100,000 loan, one point would be $1,000. how do reverse mortgages work?. Mortgage points are basically a kind of prepaid interest you can select to pay up front in exchange for a lower rates of interest and monthly payments (a practice known as "purchasing down" your interest rate). The smart Trick of How Do Split Mortgages Work That Nobody is Talking About

In exchange for each point you pay at closing, your home mortgage APR will be lowered and your month-to-month payments will diminish accordingly. Normally, you would purchase indicate reduce your rates of interest on a fixed-rate home loan. Buying points for adjustable rate home mortgages just provides a discount rate on the initial fixed duration of the loan and isn't generally done (how do reverse mortgages work?). The longer you prepare to own your new house, the better the opportunity that you'll reach the "break-even" point where the interest you've saved makes up for your initial cash outlay. If you have a shorter-term strategy, have actually limited money, or would benefit more from a larger deposit, paying points may not benefit you. The points are factored into your closing cost, and can reduce your APR, or interest rate, which is your home mortgage rate of interest plus other costs connected with your home mortgage, like any charges. (The APR is the rate at which you can expect your payments to be computed from.) Points for variable-rate mortgages are used to the fixed-rate period of the loan. Not known Facts About How Do Canadian Mortgages Work

There isn't a set amount for one point, however. For example, if you have a 5% interest rate, buying one point may lower the interest rate to 4. 75% or 4. 875%, depending upon your loan provider's terms. If you're buying mortgage points, you can purchase more than one, or perhaps a portion of one, if the lending institution allows it. If you have an interest in home loan points and lowering your rates of interest, ask your lender for a rate sheet to see the interest rates and matching home loan points. Even better, you should ask the lender for the particular dollar amount you 'd have to pay to reduce your mortgage rate by a specific percentage, considering that points (and portions of points) wesley timeshare cancel can be complicated. That means home loan points get more costly the bigger your home loan is. For example, if you have a $100,000 loan, one point will cost $1,000. however if you have a $500,000 loan then a home loan point would cost $5,000. The method mortgage points work is that the (which is however much your home mortgage points expense).

Some Of How Do Reverse Mortgages Work When You Die

More on that later on. The best way to comprehend how points work is through an example. Let's say you're securing a 30-year fixed-rate home loan for $300,000 and you're offered a 5. 00% interest rate. According to the rate sheet from your lending institution, reducing the rate of interest by 0. 25% would cost one point. No points1 pointCost of pointsNA$ 3,000 Home mortgage rate5. 00% 4. 75% Month-to-month payment$ 1,610$ 1,565 Month-to-month savingsNA$ 45. 00Total interest expenses after thirty years$ 279,671$ 263,373 Total interest cost savings after 30 yearsNA$ 16,343 We got the numbers using our mortgage calculator, which reveals your monthly payments. Examine it out to see just how Find more information much house you can pay for. Whether or not it is clever to purchase home loan points is based on your specific scenarios. If you do have the cash, then it's time to do some mathematics in order to choose whether purchasing discount points and reducing your regular monthly mortgage costs through a lower rate is the very best usage of that money. Financial calculators, like a home mortgage points calculator, can tell you the length of time it will take you to recover cost or begin saving if you buy home loan points. Indicators on How Do Home Mortgages Work You Need To Know

As the example shows, buying one point on a $300,000 loan can save you thousands of dollars in interest payments in the long run. But those savings don't start right now vacation ownership interest because of the upfront expense of $3,000. Customers will would like to know when the actual savings start that make the expense of purchasing home loan points worthwhile. To compute the break-even point using our example: the expense of home loan points ($ 3,000) divided by the monthly savings ($ 45) = 67 months. That implies purchasing points won't conserve you money until after 5 years and 7 months (67 months) into the life time of the mortgage. For reference, a 30-year home loan lasts 360 months. |

AuthorWrite something about yourself. No need to be fancy, just an overview. Archives

July 2022

Categories |

RSS Feed

RSS Feed