|

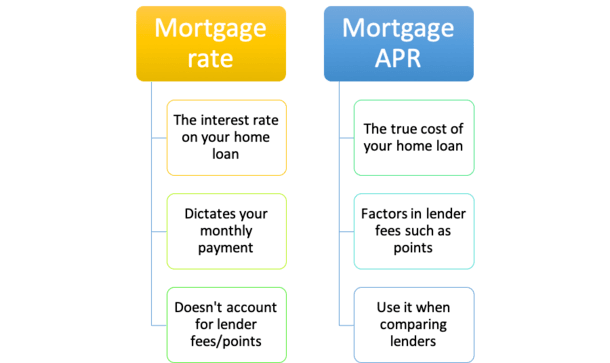

Customer might open eligible KeyBank accounts to get approved for the rates of interest discount. Regular monitoring and cost savings account service charges use. Describe particular monitoring or savings account disclosures for information. For fixed-rate home loans, the 0. 25% rate discount rate is a long-term rates of interest reduction that will be reflected in the Promissory Note interest rate. 25% rate discount will use to the initial fixed interest rate period and will be reflected in the optimum amount the rate of interest can increase over the regard to the loan, subject to the minimum rates of interest that might be charged per the regards to the Promissory Note. Rate of https://jaidenaknf178.weebly.com/blog/how-do-conventional-mortgages-work-fundamentals-explained interest discount rate might not be readily available for all products - what is the current interest rate for home mortgages. Ask us for details. Home Mortgage Terms & Conditions: The Annual Percentage Rate (APR) is the cost of credit over the term of the loan revealed as an annual rate. The APR revealed is based on interest rate, points and particular estimated finance charges. Your real APR may be various. Investment items provided through Secret Financial investment Services LLC (KIS), member FINRA/SIPC and SEC-registered financial investment consultant. Investment items offered through KIS are: NOT FDIC GUARANTEED NOT BANK ENSURED MIGHT DECLINE NOT A DEPOSIT NOT INSURED BY ANY FEDERAL OR STATE GOVERNMENT COMPANY KIS and KeyBank are different entities, and when you buy or offer securities you are doing service with KIS and not KeyBank. Lenders consider lots of elements prior to they calculate an interest rate. These elements can impact the interest rate you may get to purchase or re-finance a house or get cash from your house equity. The Fed Funds Rate (that is, the interest rate at which depository organizations lend money to each other over night) is set by the Federal Reserve Board. Lower rates normally suggest you'll pay less interest. Remember that home loan rates can vary daily. Register for Watchful eye text alerts. People with higher credit history generally get better interest rates than individuals with lower credit history. Many financial professionals recommend you look how to sell my timeshare for ways to improve your credit rating before you apply for a home mortgage or re-finance your home. 5 Simple Techniques For What Is The Interest Rate On Mortgages Today

Points are a method to "purchase" a lower interest rate. One point is equal to 1% of the loan amount. For example, on a $200,000 home mortgage, one point for that home mortgage would cost $2,000. Be aware of offers that reveal a low interest rate however require you pay points. To much better comprehend the total expense of a home mortgage offer, take a look at its yearly percentage rate. Loan term can impact rate of interest. Longer term loans generally have higher interest rates than home loans with much shorter terms. A shorter-term loan might lower your rate of interest and conserve you cash over the life of the loan. There are lots of kinds of loans you might get to buy a house, refinance a house, or get cash from your home equity. Traditional loans are provided by private loan providers without federal government support. The rates of interest you might get can vary by the kind of loan. When loans have a set rate, the quantity of money you pay in interest remains the same. When loans have an adjustable rate, the amount of cash you pay in interest can change gradually. To find out more, see our article on fixed and adjustable rate home loans. The size of your loan can impact the mortgage rate. In some cases lenders charge a greater rate of interest to individuals who desire to borrow larger amounts of cash than the common customer. These home loans are often called "jumbo loans." When you are buying a home, the quantity of your deposit can influence your home loan rate. Lenders see those able to make larger down payments as less risky. Larger deposits suggest less chance you'll leave your home and lose the worth of your down payment. Another way to consider a deposit's influence on your home loan rate is to calculate a loan-to-value ratio (or "LTV").

For instance, if you want to buy a $250,000 house with a $50,000 down payment and a $200,000 home mortgage, then your LTV is 80%. (That is, $200,000 $250,000 = 0. 80 or 80%.) Lenders tend to see mortgages with higher loan-to-value ratios as more risky than home loans with lower LTVs, and numerous charge greater rate of interest as a result. Some Of What Are The Debt To Income Ratios For Mortgages

Lenders consider your home's fair market price to determine your Click for more info loan-to-value ratio during a re-finance considering that your house's value might have changed because you purchased or last refinanced. For example, if the house you bought for $250,000 is now worth $300,000, and you owe $180,000 on the mortgage, then your LTV is 60%. 60 or 60%.) Lenders normally see refinance loans with lower loan-to-value ratios as less dangerous, and may provide a lower rate of interest as an outcome. Keep in mind that squander refinances tend to increase your LTV. With a squander re-finance, you replace your current home loan with a new home loan for a higher amount and get the difference in money at closing.

That implies the amount of your new home mortgage will be $210,000 and your LTV will be 70%. ($210,000 $300,000 = 0. 70 or 70%.) This greater loan-to-value ratio might impact your mortgage rates of interest. Freedom Home loan clients can log into their accounts to see if they have a current interest rate deal. In order to participate, the debtor should agree that the lender, Quicken Loans, might share their information with Charles Schwab Bank and Charles Schwab Bank will share their info with the loan provider Quicken Loans. Nothing herein is or need to be analyzed as an obligation to lend. Loans undergo credit and security approval. This deal undergoes alter or withdraw at any time and without notification. Rates of interest discount rates can not be integrated with any other offers or rate discounts. Risk insurance might be required. 1. Loans are eligible for only one Financier Benefit Prices discount per loan. Select mortgage are qualified for a rates of interest discount of 0. 750% based upon certifying assets of $250,000 or higher. Discount for ARMs applies to preliminary fixed-rate duration only. Certifying possessions are based on Schwab brokerage and Schwab Bank combined account balances, including: a) Brokerage accounts in which the debtor(s) is an owner, trustee or custodian; b) Conventional, Roth, and Rollover Individual Retirement accounts (IRA)* - individually owned or acquired. The Main Principles Of What Banks Use Experian For Mortgages

(Omitting Business Retirement accounts such as Simple IRA, SEP Individual Retirement Account & Pension Trust). * Customers of Independent Financial Investment Advisors: IRA account balance eligibility is not available for customers of independent financial investment consultants. Qualifying assets are based upon Schwab and Schwab Bank combined non-retirement account balances. For extra information please check out and log into www.

0 Comments

This can be different when it comes to jumbo reverse home mortgages, taken out on estates valued at $1 million or more. Families of the customers of these home mortgages need to consult loan providers to examine the contracts for the fine print on repayment. With reverse home loans, the staying balance may still be owed. Because case, a kid or relative can get a new home mortgage after the original property owner dies. The estate can also redeemed your house from the lending institution at 95% of its value. All of this needs to be done within six months, however. Even as that's going on, the reverse mortgage balance gets bigger. Often, partners go in on a reverse home loan together. In http://brooksxave348.tearosediner.net/how-do-mortgages-work-in-germany-fundamentals-explained this case, the death of one house owner does not bring the lending institutions down on your head. The loan doesn't require to be repaid till both property owners vacate the home or pass away. This also uses if one partner has to live in a care facility. Due to this, it's recommended by the Customer Financial Protection Bureau to co-borrow on reverse mortgages between 2 partners. If you do not, your partner or heir may have to pay the loan back instantly when you die. Non-borrowing spouses will need to pay back reverse mortgages within 6 months if the debtor passes away. Fascination About What Percentage Of National Retail Mortgage Production Is Fha Insured Mortgages

At that time, the loan provider sends the homeowners a due and payable notice for the loan quantity, which the customers require to react to within one month. At that time, the debtors have 6 months to settle the reverse home mortgage. Customers can likewise ask for two 90-day extra extensions to settle the loan if they need it. Nevertheless, these loans need to be paid back ultimately, so borrowers need to understand how these loans work after they have actually passed away. Often, your home will be sold, and the profits will go towards the loans. Making it through member of the family will have 30 days to react to the lending institution's initial demand, followed by a payment duration of 6 months, or an optimum of 12 months by request. Those who are getting old and have reverse mortgages and those who are part of the estate of someone who does can both gain from the details presented here. Producing a timeline of action and payment is important when reverse home loans end up being due. // What to Do About a Reverse Home Loan After Death: Reverse Mortgage Successors Duty Managing all of the obligations of an estate after death can be incredibly difficult. If your member of the family had a reverse home mortgage and you are the successor, it is essential to rapidly determine what to do about the reverse home mortgage after death. The Ultimate Guide To What Bank Keeps Its Own Mortgages

Reverse mortgages enable homeowners aged 62 and older to convert a portion of their home equity into tax-free loan proceeds, which they can elect to get either in a single lump-sum payment, in monthly installments, or through a credit line that enables funds to be withdrawn as required (who took over abn amro mortgages). The majority of reverse home loans readily available today are known as House Equity Conversion Mortgages (HECMs) - what act loaned money to refinance mortgages. Department of Real Estate and Urban Development (HUD). Reverse mortgages do not need borrowers to make monthly payments toward the loan balance as they would under a standard "forward" home loan. Nevertheless, customers are still required to pay real estate taxes, utilities, danger, and flood insurance premiums while they have a reverse home mortgage. The reverse mortgage loan balance becomes due and payable when the customer either dies or otherwise permanently leaves the home for a period longer than one continuous year, which includes moving to a different home, in addition to moving into an assisted living facility or nursing house. While reverse home mortgage holders do not have a month-to-month home loan payment, it is necessary to keep in mind the loan also ends up being due if you stop paying your residential or commercial property taxes or house owners insurance, or if you stop working to keep the property in good repair work. Nevertheless, the most common reason a reverse home mortgage becomes due is when the debtor has died, says Ryan LaRose, president and chief running officer of Celink, a reverse home mortgage servicer. Once the cancel timeshare contract reverse home mortgage is due, it needs to be paid back completely in one lump amount, LaRose says. Facts About How Much Is Mortgage Tax In Nyc For Mortgages Over 500000:oo Uncovered

Following the death of the borrower, the reverse mortgage loan servicer will send out a Condolence Letter to all known beneficiaries. This letter supplies information to the heirs and debtor's estate about the alternatives readily available to them for satisfying the reverse home loan balance. Keeping routine communication with the customer's reverse home mortgage servicer is vital during this process. " If we do not understand what's going on, we need to presume the worst that they have no intentions of settling the loan." So keeping in close contact with the servicer can really be a benefit to the heirs or those responsible for the borrower's estate. "The sooner you can call the servicer, the more time you're going to have [to settle the loan], which suggests the more choices that are on the table," according to LaRose. By doing so, the estate has the ability to sell the home to an unassociated third party for 95% of the house's current assessed worth, less any customary closing costs and real estate agent commissions. Considering that reverse home loans are "non-recourse" loans, successors will never be needed to pay more than 95% of the home's assessed worth even if the loan balance grows to surpass the worth of the house. Successors are needed to send documents to the servicer, consisting of a letter detailing their intents with the property and a copy of the realty listing, to name a few crucial documents (how to reverse mortgages work if your house burns). In whatever manner the heirs or estate strategy to please the reverse home loan balance, they need to bear in mind particular timelines required under HUD guidelines. What Can Mortgages Be Used For - The Facts

The more frequent interaction in between the estate and the loan servicer, the less opportunity for surprises. As long as the estate remains in regular interaction and has actually offered the servicer with the required paperwork, HUD guidelines will permit them time extensions for up to one year from the date of the customer's death. On the occasion that the estate is uncooperative or unresponsive to ask for information, the loan servicer does not need to wait the complete 12 months to start foreclosure. If the estate is unable to pay the loan balance or hesitates or not Homepage able to finish a deed in lieu of foreclosure within the 12-month period, then the servicer is needed to start foreclosure in an effort to acquire the title of the property. Such allowances may differ on a case-by-case basis, which is why it's important to keep the lines of communication open with the loan servicer. Remaining in constant communication with the reverse mortgage servicer can help extend the amount of time beneficiaries need to repay the loan. When requesting an extension, heirs should contact the servicer and supply paperwork, such as a letter of hardship that details their objectives to pay back the loan, a property listing, proof that they're trying to acquire funding to keep the house, or probate documents. 99% 4. 159% Source: U.S. Dept. of Housing and Urban Development, 2015 With their unique requirements and terminology, FHA mortgages can be a little confusing and intimidating. These loans are a bit different from standard mortgages due to the fact that they are government-backed. Knowing these differences can help you avoid home mortgage incidents and get much better offers for your financing. Click on the links to check out subjects more extensive. Homeownership has long been thought about the cornerstone of the American Dream. The bulk of U.S. people are house owners, and for lots of, residential or commercial property is their primary source of wealth. Yet, before the FHA was created in 1934, the United States was a country of occupants. These requirements made it tough for many people to own homes. The FHA was created to help the U.S. emerge from the Great Depression and to help Americans purchase houses. In 1965, it entered into the U.S. Department of Real Estate and Urban Development (HUD). Over the years, the realty and mortgage markets have changed substantially, and FHA programs have continued to evolve to support American homebuyers and homeowners. Typical 2018loan quantity Percentage of FHA purchase loans to newbie purchasers in 2018 83% 8 million Sources: FHA Single-Family Origination Trends Report, August 2018; FHA Annual Mgmnt Report, 2018 FHA underwriting standards, eligibility requirements and insurance coverage premiums alter all the time the agency need to stabilize the requirements of homebuyers with a required to safeguard taxpayers from losses.

The 10-Minute Rule for Mortgages Or Corporate Bonds Which Has Higher Credit Risk

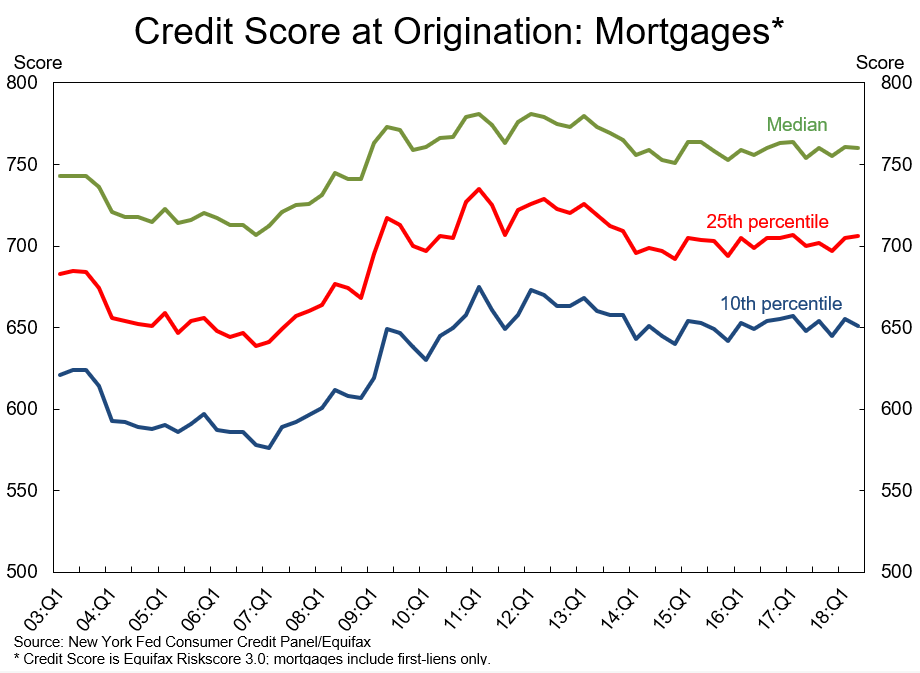

For example, in early 2008, prior to the financial crisis, nearly half of the authorized FHA loans went to customers who had a FICO score below 620, according to the FHA's 2014 annual report to Congress. The Great Economic crisis and home mortgage foreclosure crisis have pushed that percentage down to less than 5 percent of authorized debtors, as you can see in among the charts below. FHA's Market Share Because Year 2000 Source: Federal Real Estate Administration 2015 FHA Customers Credit Report Distribution Source: Federal Housing Administration 2015 You ought to understand that average credit scores are simply that averages. FHA lending institutions take a look at the whole application package payment history, earnings stability, possessions, down payment and more. Lower ratings are not constantly the result of bad credit, and lending institutions recognize that. what is the concept of nvp and how does it apply to mortgages and loans. Candidates with higher debt-to-income ratios, smaller sized deposits or other weak points typically need ratings that exceed the bare minimums. The FHA program is not the only alternative for people with small down payments who want to purchase homes. Here are other alternatives you can check out. Both Fannie Mae and Freddie Mac deal 97 percent home loans to qualified first-time property buyers. However, they have a few benefits over FHA loans: The down payment is just 3 percent. There is no upfront home mortgage insurance coverage, and the annual premiums are lower. Customers can ask for mortgage insurance coverage cancellation when the loan balance drops hyatt timeshare to 80 percent of the original house worth. If you have actually owned a house in the last three years, you don't qualify for this loan but you might still be able to get a standard loan with a 5 percent down payment. The 2-Minute Rule for What Do I Need To Know timeshare pros and cons About Mortgages And Rates

Some house sellers are willing to fund their own residential or commercial properties. The buyer may have the ability to prevent lender charges and other homebuying costs like title insurance coverage. Sellers may be more prepared than home mortgage loan providers to ignore credit or income issues. Nevertheless, buyers of owner-financed houses must have an appraisal done to prevent paying too much for the property. Private sellers do not need to play by the same rules as licensed home loan lenders, which indicates that borrowers have less defenses. FHA is not the only federal government home loan program. VA and U.S. Dept. of Agriculture (USDA) mortgage provide a variety of advantages over FHA loans for those who are qualified.

Department of Veterans Affairs guarantees home mortgages for eligible service members, veterans, and in some cases relative. These loans don't have deposit requirements, and borrowers don't have to pay month-to-month home mortgage insurance. Often supplied in rural locations, USDA loans allow certified debtors to get a home mortgage without a down payment when they buy a house in a qualified location (what are cpm payments with regards to fixed mortgages rates). citizens live in neighborhoods qualified for USDA loans. USDA home mortgages have financing costs (2 percent), which can be funded, and require annual home mortgage insurance, but the premiums are lower than FHA insurance. The FHA home loan was developed to meet the requirements of homebuyers who have smaller sized deposits it does not matter the number of houses they have actually owned. The Only Guide for How Many Va Mortgages Can You Have

A buyer with a smaller sized deposit may still be much better off with a standard loan it really depends upon the total package. what were the regulatory consequences of bundling mortgages. Property buyers ought to compare the overall costs of conventional and FHA uses from completing lending institutions to ensure they are picking the lowest-cost option that finest meets their unique requirements. Both FHA and standard home mortgage rates are set by private loan providers, not the government. Costs and rates differ among mortgage loan providers by an average of 0. 25 to 0. Half. Rates and terms can alter frequently. Home mortgage insurance costs likewise alter over time. Property buyers with less than 20 percent down should compare both standard and FHA loans when they look for home loans. There is no absolute rule because FHA home mortgage are made by private home loan lending institutions, and they set their own rates and fees. FHA lenders might likewise enforce higher http://cashhcbk444.tearosediner.net/the-smart-trick-of-how-do-mortgages-payments-work-that-nobody-is-discussing standards than the FHA requires these standards are called overlays. FHA mortgage underwriting is a few of the most forgiving in the business. 5 percent loan), proven income that is continuous, enough and stable, funds to cover the down payment and closing costs, and a debt-to-income ratio that does not exceed 43 percent. Those are the basics. Candidates who go beyond these minimum credentials have a much better chance at loan approval, and those who barely fulfill standards may need to work harder to get a loan. More About On Average How Much Money Do People Borrow With Mortgages ?

The majority of home mortgage (including FHA) are underwritten with automated underwriting systems (AUS), which deliver choices in seconds. Those with less typical situations consisting of no reported credit report, all-cash down payments or identity theft should be underwritten by hand, which can take longer. On average, home loans close in about 40 days. Only if the seller's representative has an unreliable view of FHA loans. Some believe that FHA needs higher property standards and needs sellers to pay purchaser's expenses not true. Others do not like the FHA Amendatory Clause, which allows buyers to cancel a purchase if the home does not assess for at least the prices. Some view FHA debtors as borderline and more difficult to authorize an impression that can be gotten rid of by getting loan approval prior to buying a home. One disadvantage of FHA mortgage is that borrowers can not drop FHA home loan insurance coverage, even when the loan-to-value ratio drops listed below 80 percent. If a property buyer keeps an FHA loan for an entire 30-year term, it could be pricey. The FBI and the U.S. Department of Real Estate and Urban Development Workplace of Inspector General (HUD-OIG) urge customers, especially seniors, to be alert when looking for reverse mortgage items. Reverse home mortgages, also called home equity conversion home loans (HECM), have increased more than 1,300 percent in between 1999 and 2008, creating substantial opportunities for fraud perpetrators. It also makes sure that, when the loan does end up being due and payable, you (or your heirs) don't have to pay back more than the value of the home, even if the amount due is greater than the assessed worth. While the closing expenses on a reverse home loan can often be more than the costs of the home equity credit line (HELOC), you do not have to make regular monthly payments to the lender with a reverse home loan. It's never ever a good concept to make a monetary choice under tension. Waiting up until a small issue ends up being a big problem reduces your alternatives. If you wait until you remain in a financial crisis, a little extra income each month most likely will not assist. Reverse home mortgages are best utilized as part of a sound monetary plan, not as a crisis management tool. Discover if you may get approved for assist with expenditures such as property taxes, house energy, meals, and medications at BenefitsCheckUp. Reverse home loans are best utilized as part of an overall retirement strategy, and not when there is a pending crisis. When HECMs were very first provided by the Department of Real Estate and Urban Development (HUD), a large proportion of customers were older females aiming to supplement their modest earnings.

Throughout the real estate boom, many older couples secured reverse home mortgages to have a fund for emergencies and extra money to delight in life. In today's financial recession, more youthful customers (frequently Child Boomers) are relying on these loans to manage their existing home loan or to assist pay for debt. Reverse home loans are distinct due to the fact that the age of the youngest customer determines how much you can obtain. How What Are Interest Rates Now For Mortgages can Save You Time, Stress, and Money.

Deciding whether to take out a reverse home loan is challenging. It's tough to approximate the length of time you'll stay in your home and what you'll need to live there over the long term. Federal law needs that all people who are thinking about a HECM reverse home loan get therapy by a HUD-approved therapy company. They will likewise talk about other choices including public and personal advantages that can assist you stay independent longer. It's important to consult with a counselor prior to speaking with a lending institution, so you get unbiased information about the loan. Telephone-based therapy is offered nationwide, and in person counseling is readily available in lots of neighborhoods. You can likewise find a therapist in your location at the HUD HECM Therapist Roster. It is possible for reverse mortgage customers to face foreclosure if they do not pay their real estate tax or insurance coverage, or keep their house in good repair (which of the following statements is true regarding home mortgages?). This is particularly a threat for older property owners who take the entire loan as a lump amount and invest it quicklyperhaps as a last-ditch effort to restore a bad circumstance. However, starting in 2015, brand-new guidelines need that reverse home mortgage applicants go through a lending institution monetary evaluation at the time of application. This is similar to the underwriting process in a traditional mortgage. The loan provider will look at credit reports, payment history, and home debt prior to initiating a loan. That's why reverse mortgage counseling pueblo bonito timeshare is so crucial. Things about Who Took Over Washington Mutual Mortgages

They will also look at your financial situation more broadly to help you determine if a timeshare vacation deals HECM is right for you. Always avoid any unsolicited deals for a reverse home loan or for assist with these loans. If you believe you or your family have actually been targeted by a fraudster, call 800-347-3735 to submit a grievance with HUD. When you first begin to learn about a reverse home mortgage and its associated benefits, your preliminary impression might be that the loan product is "too great to be real (how do mortgages work in monopoly)." After all, an essential advantage to this loan, designed for property owners age 62 and older, is that it does not need the customer to make regular monthly home loan payments. Though initially this advantage might make it appear as if there is no repayment of the loan at all, the reality is that a reverse mortgage is just another kind of home equity loan and does ultimately get repaid. With that in mind, you might ask yourself: without a regular monthly home mortgage payment, when and how would repayment of a reverse home mortgage occur? A reverse home loan is various https://dallasgmxn369.mozello.com/blog/params/post/3557688/not-known-details-about-how-do-interest-only-mortgages-work-uk from other loan products due to the fact that payment is not achieved through a regular monthly home mortgage payment over time. Loan maturity typically happens if you sell or move the title of your home or permanently leave the house. However, it might also occur if you default on the loan terms. You are considered to have permanently left the home if you do not live in it as your primary house for more than 12 successive months. Some Known Facts About How Do Reverse Mortgages Work After Death.

When any of these circumstances happen, the reverse mortgage ends up being due and payable. The most common technique of repayment is by selling the home, where profits from the sale are then utilized to pay back the reverse mortgage completely. Either you or your beneficiaries would usually take obligation for the deal and get any staying equity in the home after the reverse home loan is paid back.

A HECM reverse mortgage ensures that debtors are just accountable for the quantity their home costs, even if the loan balance surpasses this amount. The insurance coverage, backed by the Federal Housing Administration (FHA), covers the staying loan balance. In instances when heirs prefer to keep the house rather of selling it, they might choose another type of repayment. Qualifying beneficiaries might likewise refinance the home into another reverse home mortgage. A reverse home loan reward isn't limited to these options, however. If you would like to pay on the reverse home mortgage during the life of the loan, you definitely might do so without charge. And, when making monthly home loan payments, an amortization schedule can prove helpful. Prequalifying methods you have done an initial loan provider screening. Nevertheless, preapproval is the next action in the procedure. You need to provide the bank a lot more files like you're looking for the Visit website home mortgage. It deserves doing because you will get a preapproval letter from the bank, and this will show sellers and property agents that you're a serious buyer. Furthermore, you will have the ability to act quickly as soon as you discover that ideal location without needing to then look for funding." Scott Bilker of DebtSmart "On a traditional loan (Fannie Mae or Freddie Mac), the difference in rate in between a poor credit report (620) and a strong credit report (740-plus) might be as much as 3 (what is the current index rate for mortgages).

75 to 1. 25% in rates of interest. On an FHA or VA loan, the rate distinction might be up to 0. 75 in points in costs or 0. 125 to 0. 250% in rates of interest." Cathy Blocker, EVP, Production Operations of Guild Home Mortgage Business "There is not a single universal standard. You can't take a lending institution's marketed rates of interest for its best-qualified debtors and add a set premium due to the fact that you're a C credit rather of an A credit (A credit being the least amount of danger)." Nick Magiera of Magiera Team of LeaderOne Financial "There are only 2 ways to settle your mortgage fast: 1. 2. Pay more toward the home loan. That's it. Do not be tricked by biweekly mortgages since all they do is make you pay more. If you are not in a position to get a lower rate, then just increase your month-to-month home loan payment to an amount that is comfy, bearing in mind that this is money you can not quickly get back. If the expense of over night loaning to a bank increases, this generally triggers banks to increase the interest rates they charge on all other loans they make, to continue to make their targeted return on properties. As banks increase their rates of interest, other loan providers or financial companies likewise tend to increase their rates. Getting The What Is The Current Libor Rate For Mortgages To Work

On a $200,000 loan, 2 points suggests a payment of $4,000 to the lender. Points belong to the cost of credit to the borrower, and in turn become part of the investment go back to the lender. That said, points are not constantly required to obtain a home loan, however a 'no point' loan may have a greater rate of interest." Nick Magiera of Magiera Team of LeaderOne Financial "' Discount rate points' describes a fee, typically expressed as a portion of the loan amount, paid by the purchaser or seller to reduce the buyer's interest rate." Cathy Blocker, EVP, Production Operations of Guild Home Loan Business "Fannie Mae and Freddie Mac are the 2 most typical GSEs purchasing home mortgages from banks and home loan loan providers.

home mortgage market. They are different business that contend with one another and have really similar service models. They buy home mortgages on the secondary home mortgage market, swimming pool those loans together, and after that offer them to financiers as mortgage-backed securities outdoors market. There are subtle differences, but the primary difference in between Fannie and Freddie comes down to who they purchase mortgages from: Fannie Mae primarily buys home loan from large industrial banks, while Freddie best way to get rid of timeshare Mac mostly purchases them from smaller banking institutions (thrifts). housing economy, permitting individuals getting out of a timeshare to afford the purchase of a home, which would otherwise be impossible if Fannie and Freddie were nonexistent. Ginnie Mae basically performs the exact same function as Fannie and Freddie, except they focus on government-insured home mortgages such as FHA and VA." Nick Magiera of Magiera Team of LeaderOne Financial "Besides principal and interest, residential or commercial property taxes, danger insurance, and house owners' association fees (if applicable), there may be private home loan insurance coverage for a standard loan or month-to-month mortgage insurance coverage for an FHA loan. When I got my house, it wasn't long prior to the basement flooded, and it took thousands to install a French drain system. There is always something that requires attention, and the expenses can add up. So be sure to prepare for these circumstances. That indicates when purchasing a home, purchase less, much less, than you can afford this method, you'll remain in good condition when (not if) things require upkeep." Scott Bilker of DebtSmart "Every home purchase differs, however here's a list of the most typical documents that we'll need to validate: Previous 2 years of tax returns, past two years of W-2s or 1099s, past two months of bank statements, past thirty days of pay stubs, copy of your driver's license, copy of either your passport or Social Security card." Nick Magiera of Magiera Group of LeaderOne Financial "Not if there is a lending institution included. Sure, you might not drown, however picture what would occur if you began to sink? You need something there to secure you." Tracie Fobes, Penny Pinchin' Mama "No, no, and absolutely no it's not optional. You always want property owners insurance because anything can occur, and it will, from hailstorms that can chip away at your siding to high winds and flooding, plus other unpredicted accidents. If you're going to be accountable for paying a home mortgage for the next thirty years, you must understand exactly what a home mortgage is. A home loan has three basic parts: a deposit, month-to-month payments and fees. Considering that home loans generally involve a long-term payment plan, it is very important to understand how they work. The Ultimate Guide To How Many Mortgages Can You Have At One Time

is the quantity needed to settle the home loan over the length of the loan and consists of a payment on the principal of the loan as well as interest. There are often property taxes and other costs included in the monthly expense. are various costs you need to pay up front to get the loan. The bigger your deposit, the better your funding deal will be. You'll get a lower home loan rate of interest, pay less charges and get equity in your house more rapidly. Have a lot of concerns about mortgages? Take a look at the Customer Financial Protection Bureau's answers to regularly asked questions. There are two main types of home mortgages: a traditional loan, guaranteed by a private lending institution or banking organization and a government-backed loan. This gets rid of the need for a deposit and likewise avoids the need for PMI (personal mortgage insurance coverage) requirements. There are programs that will assist you in getting and funding a home loan. Contact your bank, city advancement office or a well-informed property representative to discover more. A lot of government-backed home mortgages been available in among 3 types: The U.S. The first step to get a VA loan is to get a certificate of eligibility, then send it with your latest discharge or separation release papers to a VA eligibility center. The FHA was developed to assist individuals acquire economical housing. FHA loans are actually made by a loan provider, such as a bank, but the federal government insures the loan. If you're able and willing to move, selling your home and moving to a smaller, cheaper one can offer you access to your existing home's equity. You can utilize the earnings of the sale to spend for another home in cash or pay off other financial obligation. If you haven't paid off your home loan yet, you might look into re-financing the loan to reduce your regular monthly payments and free up the distinction - what were the regulatory consequences of bundling mortgages. As you purchase a reverse home loan and consider your choices, watch for two of the most typical reverse home mortgage scams: Some professionals will try to encourage you to get a reverse home loan when touting home improvement services. The Department of Veterans Affairs (VA) does not provide reverse home loans, however you may interval international timeshare see advertisements assuring unique offers for veterans, such as a fee-free reverse home loan to bring in customers. If a specific or business is pushing you to sign a contract, for instance, it's most likely a warning. A reverse home loan presents a way for older homeowners to supplement their income in retirement or spend for house remodellings or other expenditures like health care expenses. There are eligibility requirements that define who can take advantage of this kind of loan, just how much money can be gotten and what the homeowner has to do to remain in excellent standing. A therapist can help describe the advantages and disadvantages and how this kind of loan may impact your beneficiaries after you pass away. To locate an FHA-approved lending institution or HUD-approved therapy firm, you can visit HUD's online locator or call HUD's Real estate Counseling Line at 800-569-4287. The FBI and the U.S. Department of Real Estate and Urban Advancement Office of Inspector General (HUD-OIG) desire consumers, particularly seniors, to be vigilant when looking for reverse home loan items. Reverse mortgages, also known as home equity conversion home loans (HECM), have actually increased more than 1,300 percent in between 1999 and 2008, developing considerable chances for fraud criminals. Everything about What Are Interest Rates On Second Mortgages

In between 2013 and 2017, nearly 100,000 reverse mortgages have failed. California was struck particularly tough with lending institutions foreclosing at a rate two to three times the nationwide average. Many senior citizens have actually turned to a reverse mortgage to money their retirement years by accessing the equity in their houses. The problem is, a number of these debtors didn't understand that reverse mortgage foreclosure is possible. What Is a Reverse Home mortgage and How Do They Work?A reverse mortgage lets homeowners over the age of 62 obtain against the equity developed in the home. This provides an instant injection of money in exchange for equity. The homeowner need to continue to pay the insurance coverage and real estate tax. Usually, the debtor's estate repays the loan by offering your house. Reverse home loans are non-recourse, so there's no liability if the house's sale profits do not totally pay back the loan. When Is a Reverse Home mortgage Foreclosure Possible?When people believe of foreclosure, they think about a conventional mortgage where the debtor stopped working to make their regular monthly payments. Some situations result in foreclosure as a natural part of the procedure. This takes place if the balance owed is higher than the home's worth, or there's no one to deal with the sale. The estate will let your home enter into foreclosure. Then there are the foreclosures that take place while the borrower is still alive. If the customer moves out before the needed time, the loan grows and ends up being due. The lender will provide the customer a defined amount of time to repay the loan, and if that does not take place, the lender will foreclose. Failure to Pay Taxes or InsuranceProperty owners are needed to stay current on both taxes and insurance - how to reverse mortgages work if your house burns. All About How To Hold A Pool Of Mortgages

The lending institution's reaction will be to foreclose on the house. What You Can Do to Prevent ItIf you're dealing with reverse home mortgage foreclosure, you need to look for legal representation instantly. Your attorney can work with the lending institution to protect loan adjustment or mitigation. They can find out a way to work with the loan provider to guarantee you remain in your house.

However, if your financial challenge is beyond your control, you might wind up dealing with foreclosure. If you're dealing with reverse home mortgage foreclosure, then the best thing you can do is talk to an attorney. They will have the ability to explain all of your choices and communicate with the lender for you. Share this story Released November 17th, 2020 at 11:00 AM Above image credit: A home. (Photo Adobe) Carl Abrams has owned his house since 1989. Now 78, about four years back, he got a reverse home mortgage that's a loan for people 62 and older that turn a home into money prior to they move or die. With a reverse mortgage, the property owner stays accountable for paying property taxes, property owner's insurance and upkeep costs. If those payments aren't made in a timely fashion, the house can go into foreclosure. Problem was, Abrams wasn't mindful he required homeowner's insurance. His reverse home mortgage servicer had force-placed insurance coverage on his home when he wasn't spending for it. Brittany McCormick, is timeshare worth it a customer lawyer at Minneapolis-based Mid-Minnesota Legal Aid, got him onto a repayment plan rather. Abrams took two years to pay it off sending out in an additional $209 a month and ending up last December. "I almost lost the home," he states. "It's been hard." Many low- and moderate-income homeowners with reverse home loans, particularly in minority areas, aren't so fortunate. A Biased View of How Is The Compounding Period On Most Mortgages Calculated

" Nine times out of 10, its [unsettled] real estate tax," says McCormick. "The home is their only asset." An U.S.A. Today investigative report in 2015 discovered that following the Excellent Economic crisis, almost 100,000 reverse home mortgages stopped working, "blindsiding https://app.gumroad.com/tricusmacn/p/indicators-on-how-do-right-to-buy-mortgages-work-you-should-know elderly customers and their households and dragging down property values in their areas." And, the examination found that low-income minority communities were most impacted by predatory reverse-mortgage lending; typically, the loans were sold through aggressive door-to-door pitches, USA Today said. The debtors who went into foreclosure in some cases lost their homes due to small financial obligations for real estate tax or loan servicing errors. Even if a fairly percentage is owed, "you might lose your house," says Joanne Savage, senior staff attorney, AARP Legal Counsel for the Elderly. Includes Matthew Hulstein, monitoring lawyer at Chicago Volunteer Legal Providers: "Whatever the reason mental health, not budgeting we see foreclosure cases for $3,000, $4,000, $5,000. A retired artist and teacher, she had a reverse home mortgage on her house, which she had actually likewise turned into an Airbnb to pay her rising real estate tax. Her Airbnb service dried up with the pandemic. She asked the company servicing her reverse home mortgage if she could delay paying the taxes, since the Irs had pressed back the filing date for income taxes this year because of COVID-19 - who provides most mortgages in 42211. The next thing she knew, her servicer declared that since she hadn't paid her home taxes, she needed to settle her loan in full or enter into foreclosure. McCormick fixed the "silly error" on the part of the servicer with a few quick telephone call. Crisis prevented and apology accepted. There are lots of home mortgage loan providers that now offer what they call digital or online home mortgages. However the reality is, many people who use for online home loans will frequently have to talk to a loan officer and will usually require to receive physical copies of their home mortgage documents and sign these papers during a standard mortgage closing, generally at a title company's workplace. You may need to obtain a mortgage with a loan officer who can take your uncommon situations into account when figuring out whether you certify. However there is no denying that online tech is slowly streamlining the mortgage process. And while there is still a need for the human component, online loaning is easing a minimum of some of the headaches related to making an application for a loan. Today, however, customers who are used to online food delivery, ride-sharing apps and Web banking, are significantly demanding that loan providers automate more of the home loan process. "For a long time, the home mortgage industry has actually been seen as stagnant and loaded with human error. Property buyers have associated the home loan get out of timeshare process with stress and disappointment," Jacob said. Online lenders likewise enable debtors to submit their property loan applications at their web sites, removing the requirement to mail, drop off or fax this completed form to a physical place. These changes can save time. Jacob stated that it can take conventional mortgages approximately 45 days to close.

Tom Furey, co-founder and senior vice president of item development, finance and financing, with Stone, Colorado-based Neat Capital, stated that online mortgages are typically less pricey. That's since companies like his-- Cool offers digital home loans-- utilize technology to remove the inadequacies of the traditional mortgage-lending process. This results in faster closing times and less administrative costs, Furey stated. " Underwriting takes place in the background weeks after customers receive a pre-approval." Neat Capital relies on what Furey calls a digital real-time approval system that asks specific concerns of customers. Furey says that Neat Capital's application engine may ask for how long a customer will get income from alimony payments or the length of time they have actually made a certain series of self-employment income. However rather of needing borrowers to discover copies of their income tax return or print out copies of their checking account declarations, Neat utilizes connecting technology to verify the assets of the majority of its customers instantly, scanning the connected bank accounts and retirement funds of these buyers to identify how much money they have in each of them. More About Who Has The Best Interest Rates For Mortgages

Borrowers who fidget about connecting their accounts have the alternative of publishing PDF versions of their declarations, and Neat will only pull data from connected accounts if their customers provide their approval. This connecting procedure, though, does speed the lending process, and spares borrowers from having to make copies of their income tax return, bank statements, retirement fund balances and credit card declarations. Furey stated that the company does use these human home mortgage experts in case borrowers do have questions and require to talk to a loaning professional. "It's likely the biggest purchase an individual will ever make, so it's crucial they feel supported," Furey said. Josh Goodwin, creator of Tampa, Florida-based Goodwin Home mortgage Group, states that while online mortgage financing is convenient and typically features lower home loan rates of interest and fees, it's not perfect - why reverse mortgages are a bad idea. State you make a significant chunk of your income from freelance work. You might require to speak with an actual human loan officer so that you can discuss why this work, though freelance, is steady, indicating your long history of agreement work as evidence. The exact same may be real if you just recently suffered a temporary reduction in your yearly earnings. But if you meet a loan officer face to face, you can explain that your income drop was only short-term, and that you have since landed a brand-new, higher-paying task. Goodwin stated that borrowers without perfect credit or with odd income streams may do much better to make an application for a loan the old-fashioned way, by meeting, or at least speaking by phone, with a mortgage officer. That loan provider approved the debtor for a loan of just $68,000. When that same borrower concerned Goodwin, he was able to authorize him for a loan of $280,000. As Goodwin says, meeting in individual with a loan officer can lead to a more customized mortgage-lending experience. "The whole homebuying process can be a difficult experience for numerous purchasers," Goodwin stated. Debtors might think that all online lenders can Click here for more run in all 50 states. This isn't always the case. Neat Capital lists the states in which it can run on its homepage. The company also includes a link to the NMLS Consumer Gain access to site, a site that lets borrowers browse for loan officers and determine where they are certified to do business. Simply because you begin a home mortgage application online, doesn't mean that you'll never ever meet in individual with lending specialists such as a loan officer or title agent. Think about the closing process. According to the 2018 J.D. Power Main Home Loan Origination Study, almost half of all consumers report receiving their closing files as a difficult copy face to face, while another 3rd receive them as hard copy through the mail. How To Combine 1st And 2nd Mortgages Things To Know Before You Buy

Power, stated that the majority of loan closings still occur in a title business workplace, in individual, with the homebuyers signing the essential paperwork to complete the home loan "Lenders and customers all have some level of confusion and distinction of opinion about exactly what constitutes a 'digital home mortgage,'" Cabell said. Cabell stated that the J.D. Cabell said, too, that customers mention a greater level of fulfillment when using a mix of individual and self-service. It might make one of the most sense, then, for borrowers to work with loan http://donovankvrc860.bearsfanteamshop.com/an-unbiased-view-of-how-do-interest-only-mortgages-work providers who allow them to complete loan applications online and send loan files through an online website but also provide access to knowledgeable loan officers who can assist walk them through the lending process (what kind of mortgages are there). Shopping around for a mortgage or mortgage will assist you get the best funding offer. A home mortgage whether it's a home purchase, a refinancing, or a home equity loan is an item, just like a vehicle, so the cost and terms might be negotiable. You'll want to compare all the expenses involved in acquiring a home mortgage. Obtain Info from A number of Lenders Obtain All Important Expense Info Home loans are readily available from numerous kinds of loan providers thrift organizations, industrial banks, home mortgage business, and credit unions. Various loan providers might quote you various costs, so you ought to call numerous lenders to make certain you're getting the finest cost. You can also get a house loan through a home loan broker. A broker's access to several loan providers can suggest a broader choice of loan items and terms from which you can choose. Brokers will normally get in touch with several loan providers regarding your application, however they are not bound to discover the very best deal for you unless they have contracted with you to function as your representative. Home loan loan providers want your business and the very first deal you see may not be the very best offer you can get. It's suggested to research at least Browse around this site a couple of lenders,. compare home loan rates and choose carefully. Our home loan calculator can show you what you may receive with numerous different lending institutions, which can help you get begun. Of course, controlling some aspects that dictate your home mortgage rate are absolutely in your power. Snagging a lower rate is all about making yourself appear a more trustworthy borrower. You see, lenders charge different debtors different rates based upon how most likely each person is to stop paying( to default, to put it simply ). One way for lenders to reduce losses is with higher rates of interest for riskier debtors. Lenders have a variety of ways to evaluate prospective debtors. As a basic guideline, lenders think that somebody with a lot of savings, constant earnings and a great or better score (which indicates a history of honoring financial obligations )is less likely to stop making. payments. On the other hand, a prospective customer with a history of late or missed out on payments( a bad credit rating, simply put) is thought about a lot more likely to default. A high debt-to-income ratio is another red flag. timeshare out This is when your income isn't high enough to support your combined debt load, which can include trainee loans, vehicle loan and credit card balances. If you have bad credit, it might deserve waiting up until you improve it to look for a home loan. Many lending institutions recommend waiting, as it's the very best method to get a low home mortgage rate (that lasts the life of the loan for fixed-rate home mortgages ). It's something to think about as a financial choice. 98 Google rating, you can feel positive that your lender will treat you right. Certain platforms likewise allow you to reach out to specific customers to comprehend that circumstance better. While checking out evaluations online can be an important tool for comparing loan providers, bear in mind that they are just part of the picture, and you should not decide solely on scores. Editorial Note: Credit Karma receives payment from third-party advertisers, but that does not affect our editors' opinions. Our marketing partners do not evaluate, authorize or back our editorial material. It's precise to the best of our understanding when published. Availability of items, functions and discounts may differ by state or area. Read our Editorial Standards for more information about our team. Some Ideas on How To Qualify For Two Mortgages You Should Know

It's pretty basic, actually. The offers for financial items you see on our platform originated from companies who pay us. The money we make assists us offer you access to free credit rating and reports and assists us produce our other fantastic tools and academic materials. Payment might factor into how and where products appear on our platform (and in what order). That's why we supply functions like your Approval Chances and savings quotes. Of course, the deals on our platform do not represent all monetary items out there, but our objective is to reveal you as numerous terrific options as we can. Personal loans are installment loans, implying you obtain a certain quantity of money and pay it off in set amounts over a duration of time. Whether you're buying a new individual loan or desire to refinance one, you'll wish to compare loan offers before signing on the dotted line. Here are some crucial loan terms to compare to assist you discover the right loan for your budget and circumstances. See if you prequalify When you're obtaining money, you desire to find a loan that meets your requirements at the most-affordable terms. The interest rate on your loan is a percentage of the overall quantity you're obtaining and has a considerable influence on its cost. You might also see an annual percentage rate, or APR, in your loan offer. The APR includes the rates of interest plus loan charges, which can give you a much better sense of the loan's true cost. What Is The Current Index For Adjustable Rate Mortgages Fundamentals Explained

A variable rate can alter and potentially increase throughout your loan term. If you have great credit, you might receive competitive rates and terms that's because loan providers consider you to be a less-risky borrower. If your credit ratings aren't fantastic and you're not in a rush to borrow, think about working on your credit before applying. You'll have to ask yourself whether you wish to get a protected or unsecured loan. A guaranteed loan is backed by security, like your home or cars and truck. But if you're unable to pay a protected loan back, you might lose the home you utilized as security on the loan. An unsecured loan, on the other hand, doesn't need security, so you don't have to worry about possibly losing your residential or commercial property. Before you sign any loan deal, you'll want to check if the loan provider charges any costs they can accumulate throughout the life of the loan. Here are some common charges to watch out for. This is an upfront charge a lending institution may charge for processing your loan. For example, if you borrow $5,000 with a 1% origination charge, $50 would go toward the fee, and you 'd receive $4,950 in a check or bank deposit. Lenders might charge prepayment charges if you settle your loan early. If you're expecting a money windfall or preparing to pay off the loan ahead of schedule, check to see whether a fee will apply before devoting - what are interest rates now for mortgages. Some Known Details About What Are The Different Types Of Mortgages

On a comparable note, if your bank account often runs low, you might want to see if you'll be charged an insufficient-funds fee. You could be charged such a charge for attempting to make a payment and not having adequate money in your account to cover it. Lenders may provide short-term and long-term personal loans. For example, LightStream might let you obtain cash for as much as 12 years. However a longer term isn't always much better. A long-term loan could lead to lower regular monthly payments, however it might also indicate paying more in interest over the long run. Your monthly payment is the amount you pay every month until your loan is paid off - what are interest rates today on mortgages. However the regular monthly expense doesn't inform the entire story about the overall expense of the loan. When you're shopping for an individual installment loan, lending institutions need to have the ability to tell you the total quantity you'll need to pay, including the loan principal plus interest and fees though this omits any late charges or insufficient-funds charges you may be charged. Getting a loan with a long timeshare nyc term can reduce your regular monthly payment, which makes a loan look less expensive in the beginning glimpse. But it can also lead to a boost to your general cost. State you wish to obtain $10,000 for debt consolidation and you're comparing 2 loan alternatives. Loan quantity APR Loan term Regular monthly payments Interest paid $10,000 6% 3 years $304.

The Best Strategy To Use For Why Do Mortgage Companies Sell Mortgages To Other Banks

90 $10,000 6% 5 years $193. 33 $1,599. 68 While your loan payment is less each month if you choose the loan that has a five-year loan term, you'll end up paying more general. When you're comparing lending institutions, you'll have to choose which is more vital to you: a lower monthly payment or a lower overall expense. If you're ready to start your loan search, consider looking at prequalification choices. Some lending institutions permit you to request prequalification by informing them basic details about yourself and your financial resources. Prequalifying lets you inspect possible rates and terms frequently without a hard questions on your credit. But prequalification is not the same as approval. However prequalification can give you a concept of what terms and charges might be offered prior to you go through with a real application. See if you prequalify Taylor Medine is an indie author and expert author who covers personal finance subjects for numerous media outlets. Her work has actually been included on websites such as FinanceBuzz, Financing Learn more.. It's our objective to supply low home loan rates and a quickly, easy mortgage process from application to closing. From newbie house buyers to experienced homeowners, we want you to feel comfy and positive with the process due to the fact that the less you invest in your home mortgage, the more you can invest in the things you like!. Debtor may open eligible KeyBank accounts to get approved for the rates of interest discount. Normal checking and savings account service fee use. Describe particular checking or savings account disclosures for details. For fixed-rate home loans, the 0. 25% rate discount is an irreversible interest rate reduction that will be reflected in the Promissory Note rate of interest. 25% rate discount will apply to the initial fixed rates of interest period and will be shown in the optimum amount the interest rate can increase over the term of the loan, subject to the minimum interest rate that might be charged per the terms of the Promissory Note. Rate of interest discount may not be offered for all products - what is the harp program for mortgages. Ask us for information. Mortgage Terms & Conditions: The Annual Percentage Rate (APR) is the cost of credit over the regard to the loan revealed as a yearly rate. The APR Click to find out more revealed is based upon rate of interest, points and particular approximated finance charges. Your actual APR may be various. Investment products offered through Secret Financial investment Solutions LLC (KIS), member FINRA/SIPC and SEC-registered financial investment advisor. Investment items provided through KIS are: NOT FDIC GUARANTEED NOT BANK ENSURED MAY DECLINE NOT A DEPOSIT NOT INSURED BY ANY FEDERAL OR STATE GOVERNMENT AGENCY KIS and KeyBank are different entities, and when you buy or offer securities you are doing service with KIS and not KeyBank. Lenders think about numerous aspects prior to they determine a rates of interest. These factors can affect the rates of interest you might get to buy or refinance a house or get money from your home equity. The Fed Funds Rate (that is, the rates of interest at which depository organizations provide cash to each other over night) is set by the Federal Reserve Board. Lower rates generally mean you'll pay less interest. Remember that home mortgage rates can vary daily. Sign up for Eagle Eye text signals. People with greater credit rating typically improve rate of interest than individuals with lower credit history. Numerous monetary specialists advise you search for methods to enhance your credit history prior to you request a mortgage or re-finance your house. The Of Who Took Over Washington Mutual Mortgages

Points are a method to "purchase" a lower rates of interest. One point is equal to 1% of the loan amount. For example, on a $200,000 home mortgage, one point for that home loan would cost $2,000. Be mindful of offers that reveal a low interest rate however need you pay points. To better understand the total expense of a home loan deal, take a look at its interest rate.

Loan term can affect rate of interest. Longer term loans normally have greater interest rates than mortgages with much shorter terms. A shorter-term loan might lower your rates of interest and save you cash over the life of the loan. There are numerous types of loans you may get to buy a home, refinance a house, or get cash from your house equity. Standard loans are offered by personal lending institutions without government backing. The interest rate you might get can differ by the type of loan. When loans have a set rate, the quantity of money you pay in interest stays the same. When loans have an adjustable rate, the amount of cash you pay in interest can alter with time. To get more information, see our article on fixed and adjustable rate home loans. The size of your loan can affect the home mortgage rate. In some cases lending institutions charge a higher rates of interest to people who wish to borrow bigger amounts of cash than the normal borrower. These mortgages are typically called "jumbo loans." When you are purchasing a house, the amount of your deposit can influence your mortgage rate. Lenders see those able to make cruise timeshare larger down payments as less risky. Larger deposits suggest less opportunity you'll ignore your home and lose the value of your down payment. Another way to think about a down payment's impact on your home mortgage rate is to calculate a loan-to-value ratio (or "LTV"). For instance, if you want to buy a $250,000 house with a $50,000 deposit and a $200,000 home loan, then your LTV is 80%. (That is, $200,000 $250,000 = 0. 80 or 80%.) Lenders tend to see home mortgages with greater loan-to-value ratios as more dangerous than home mortgages with lower LTVs, and lots of charge greater interest rates as a result. Excitement About How Many Mortgages In The Us

Lenders consider your house's fair market worth to compute your loan-to-value ratio during a refinance considering that your home's worth might have changed since you purchased or last refinanced. For instance, if the home you purchased for $250,000 is now worth $300,000, and you owe $180,000 on the home loan, then your LTV is 60%. 60 or 60%.) Lenders typically see refinance loans with lower loan-to-value ratios as less dangerous, and may offer a lower interest rate as a result. Bear in mind that money out refinances tend to increase your LTV. With a squander refinance, you change your present mortgage with a brand-new mortgage for a higher quantity and get the difference in money at closing. That means the quantity of your brand-new mortgage will be $210,000 and your LTV will be 70%. ($210,000 $300,000 = 0. 70 or 70%.) This greater loan-to-value ratio may impact your mortgage rate of interest. Flexibility Home loan clients can log into their accounts to see if they have a present interest rate offer. In order to participate, the debtor should concur that the lending institution, Quicken Loans, might share their information with Charles Schwab Bank and Charles Schwab Bank will share their details with the lending institution Quicken Loans. Absolutely nothing herein is or must be translated as an obligation to lend. Loans undergo credit and collateral approval. This offer is subject to change or withdraw at any time and without notice. Rate of interest discounts can not be integrated with any other offers or rate discounts. Risk insurance coverage may be required. 1. Loans are eligible for only one Investor Benefit Pricing discount per loan. Select home loan loans are eligible for an interest rate discount of 0. 750% based upon qualifying assets of $250,000 or greater. Discount rate for ARMs applies to preliminary fixed-rate period just. Qualifying properties are based on Schwab brokerage and Schwab Bank combined account balances, including: a) Brokerage accounts in which the borrower(s) is an owner, trustee or custodian; b) Standard, Roth, and Rollover Individual Retirement accounts (IRA)* - separately owned or acquired. Not known Incorrect Statements About When Do Adjustable Rate Mortgages Adjust

(Leaving out Business Pension such as Simple Individual Retirement Account, SEP IRA & Pension Trust). * Visit the website Clients of Independent Investment Advisors: IRA account balance eligibility is not readily available for clients of independent investment advisors. Qualifying assets are based on Schwab and Schwab Bank combined non-retirement account balances. For additional information please check out and log into www. This can be different in the case of jumbo reverse home loans, taken out on estates valued at $1 million or more. Households of the debtors of these home mortgages need to examine with lenders to examine the agreements for the small print on repayment. With reverse mortgages, the remaining balance might still be owed. In that case, a child or relative can secure a brand-new home mortgage after the initial property owner passes away. The estate can also redeemed your house from the lender at 95% of its value. All of this needs to be done within six months, nevertheless. Even as that's going on, the reverse mortgage balance gets larger. Often, partners go in on a reverse home loan together. In this case, the death of one homeowner does not bring the lending institutions down on your head. The loan does not require to be repaid up until both property owners move out of your house or pass away. This likewise applies if one spouse needs to live in a care center. Due to this, it's advised by the Customer Financial Protection Bureau to co-borrow on reverse mortgages between 2 spouses. If you do not, your partner or beneficiary might need to pay the loan back immediately when you pass away. Non-borrowing spouses will have to pay back reverse home loans within 6 months if the debtor passes away. The Definitive Guide to What Is A Bridge Loan As Far As Mortgages Are Concerned

At that time, the lending institution sends out the house owners a due and payable notice for the loan quantity, which the borrowers require to respond to within 1 month. At that time, the debtors have 6 months to pay off the reverse home mortgage. Customers can also request two 90-day extra extensions to settle the loan if they require it.

Nevertheless, these loans have to be repaid eventually, so borrowers require to understand how these loans work after they have actually passed away. Typically, the home will be sold, and the profits will go towards the loans. Surviving household members will have 30 days to react to the lending institution's preliminary request, followed by a payment duration of 6 months, or a maximum of 12 months by request. Those who are getting old and have reverse home mortgages and those who belong to the estate of someone who does can both take advantage of the info presented here. Creating a timeline of action and payment is important when reverse home loans become due. // What to Do About a Reverse Home Loan After Death: Reverse Home Loan Heirs Obligation Handling all of the duties of an estate after death can be incredibly stressful. If your relative had a reverse mortgage and you are the heir, it is necessary to quickly find out what to do about the reverse home mortgage after death. All about What Is Minimum Ltv For Hecm Mortgages?

Reverse home loans enable house owners aged 62 and older to convert a part of their house equity into tax-free loan proceeds, which they can choose to receive either in a single lump-sum payment, in month-to-month installments, or through a line of credit that permits funds to be withdrawn as required (what are cpm payments with regards to fixed mortgages rates). Most reverse mortgages available today are called Home Equity Conversion Home Mortgages (HECMs) - what is the interest rate today on mortgages. Department of Real Estate and Urban Development (HUD). Reverse mortgages do not require debtors to make month-to-month payments towards the loan balance as they would under a traditional "forward" home loan. However, borrowers are still needed to pay real estate taxes, energies, risk, and flood insurance premiums while they have a reverse mortgage. The reverse home loan balance ends up being due and payable when the customer either passes away or otherwise completely leaves the house for a period longer than one continuous year, which includes transferring to a various home, along with moving into an assisted living facility or nursing house. While reverse home mortgage holders do not have a monthly home mortgage payment, it is very important to remember the loan likewise ends up being due if you stop paying your real estate tax or homeowners insurance coverage, or if you stop working to preserve the home in great repair work. However, the most typical factor a reverse home loan ends up being due is when the borrower has actually died, states Ryan LaRose, president and chief operating officer of Celink, a reverse mortgage servicer. As soon as the reverse home loan is due, it needs to be paid back completely in one lump sum, LaRose says. The Buzz on How To Compare Mortgages Excel With Pmi And Taxes

Following the death of the customer, the reverse mortgage loan servicer will send out an Acknowledgement Letter to all known successors. This letter provides information to the beneficiaries and debtor's estate about the alternatives offered to them for pleasing the reverse home mortgage loan balance. Preserving regular interaction with the customer's reverse home loan servicer is imperative throughout this process. " If we don't know what's going on, we have to assume the worst that they have no objectives of settling the loan." So keeping in close contact with the servicer can actually be an advantage to the beneficiaries or those responsible for the customer's estate. "The earlier you can contact the servicer, the more time you're going to have [to settle the loan], which indicates the more alternatives that are on the table," according to LaRose. By doing so, the estate is able to sell the residential or commercial property to an unrelated 3rd party for 95% of the home's existing appraised value, less any traditional closing expenses and realtor commissions. Given that reverse home loans are "non-recourse" loans, successors will never ever be required to pay more than 95% of the house's appraised worth even if the loan balance grows to go beyond the value of the home. Heirs are needed to submit documentation to the servicer, including a letter detailing their intents with the home and a copy of the genuine estate listing, among other crucial documents (which mortgages have the hifhest right to payment'). In whatever manner the successors or estate plan to satisfy the reverse mortgage balance, they need to be mindful of certain timelines needed under HUD rules. How Does Bank Know You Have Mutiple Fha Mortgages Fundamentals Explained

The more regular communication in between the estate and the loan servicer, the less opportunity for surprises. As long as the estate stays in regular communication and has offered the servicer with the required documents, HUD guidelines will permit them time extensions for approximately one year from the date of the customer's death. In case the estate is uncooperative or unresponsive to demands for information, the loan servicer does not need to wait the full 12 months to start foreclosure. If the estate is unable to pay the loan balance or is reluctant or not able to finish a deed in lieu of foreclosure within the 12-month period, then the servicer is needed to Click to find out more start foreclosure in an effort to get the title of the home. Such allowances might differ on a case-by-case basis, which is why it is very important to keep the lines of interaction open with the loan servicer. Remaining in consistent interaction with the reverse home mortgage servicer can assist extend the amount of time successors need to pay back the loan. When asking for an extension, heirs need to call the servicer and supply documentation, such as a letter of difficulty http://knoxfcxp451.timeforchangecounselling.com/the-8-minute-rule-for-how-do-interest-only-mortgages-work that information their intentions to pay back timeshare worth the loan, a realty listing, evidence that they're trying to get funding to keep your house, or probate documents. |

AuthorWrite something about yourself. No need to be fancy, just an overview. Archives

July 2022

Categories |

/what-caused-2008-global-financial-crisis-3306176_FINAL-5c61ad8ac9e77c000159c893.png)

RSS Feed

RSS Feed